We’re revealing how Africa’s underbanked population and mobile phones gave rise to a massive FinTech market.

M-Pesa transformed Africa. The Kenya-founded mobile-phone transfer system may not have been the only reason why the continent has seen a boom in FinTech startups. However, few would argue against the notion that it was the start of it all. “M-Pesa has fundamentally altered the landscape of financial services in Kenya and Tanzania,” the OECD said in its African Economic Outlook 2015 report.

It noted that by 2014, over 60 per cent of the population of these two countries used mobile payments thanks to M-Pesa. Today, its services are also available in India, Lesotho, the Democratic Republic of the Congo, Ghana, Mozambique and Egypt. Unsurprisingly, given the success, it has also faced the launch of several competing services popping up across the continent.

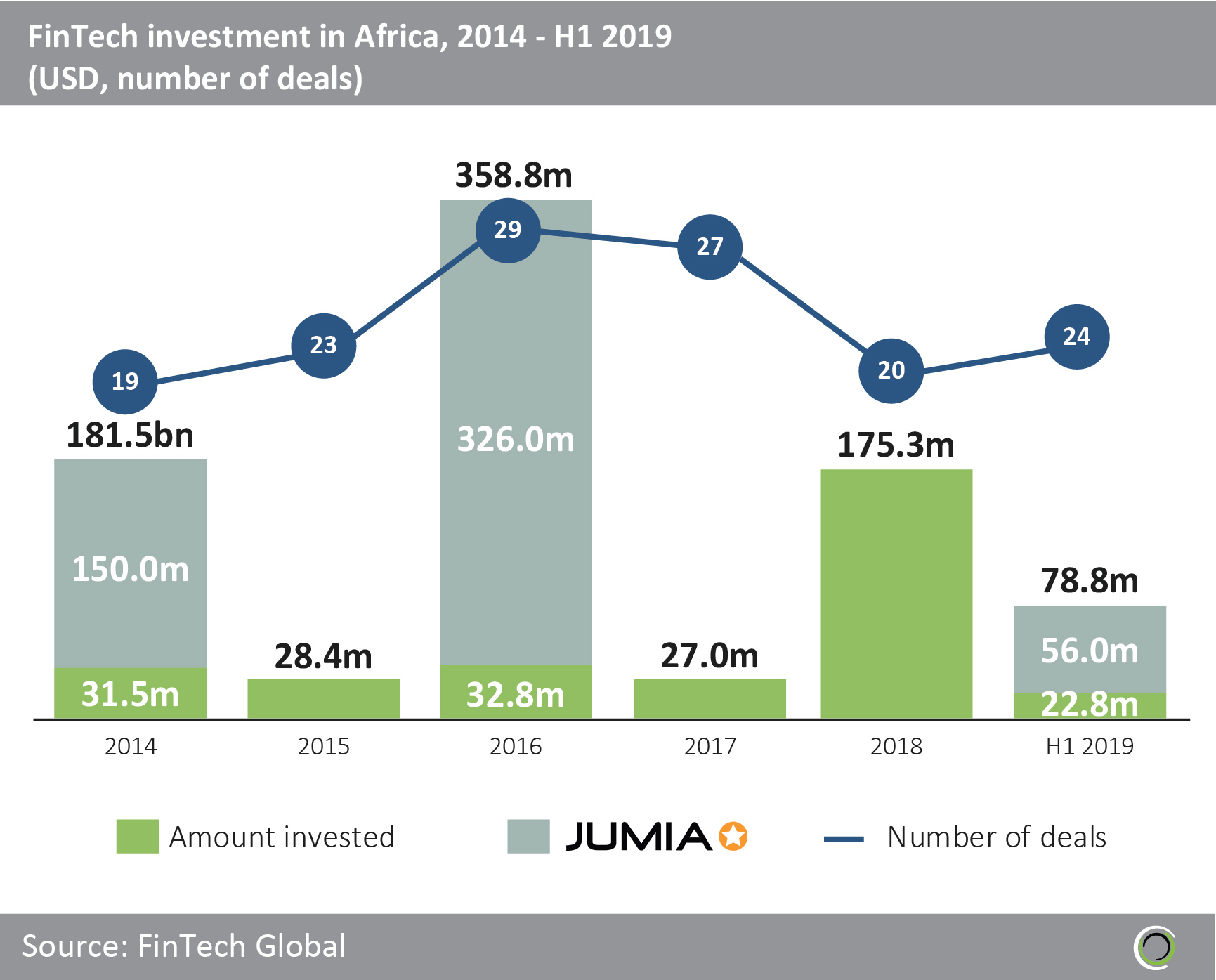

Nigeria was also the birthplace of the Africa’s only unicorn so far – the e-commerce platform Jumia. Launched in 2012, the company has raised $554.8m between 2014 and the first six months of 2019. To put that in perspective, $849.8m was invested in African FinTech businesses in total during that period, according to FinTech Global’s own research.

Now that’s something to consider given how Tunde Kehinde, co-founder and former co-CEO of Jumia Group, has described the launch of the company as five people sitting in a small room. Today the platform employs over 5,000 people in Africa. Moreover, it was officially listed on the New York Stock Exchange in April 2019.

But even without the capital injections into the e-commerce giant, investment into the continent’s FinTech industry jumped from $31.5m in 2014 to $175.3m in 2018. Nigeria, Kenya and South Africa were the three dominant capital receivers, with almost three-quarters of all deal activity in the region going into those countries.

So why is Africa experiencing such a jump in investment? Mario Marconi, co-founder and partner of Africa Wealth Partners, the African startup advisory firm, suggests it is because of mobile phones. “In reality the boom in FinTech has gone hand in hand with significant investments in telecoms as both are necessary to provide such solutions,” he says.

Marconi is not wrong. The OECD highlighted in its report that telecommunications have provided even those living remotely with mobile banking and driven economic growth. As such, more people have been able to work in transport, trade, real estate and financial services. Although, the OECD noted that many of these jobs were still in the informal market.

Still, the number of people with access to mobile phones is growing. EY, the assurance, tax, transaction and advisory services firm, noted that more than one billion people of the 1.3 billion living in Africa are expected to have access to mobile phones by 2025. The consultancy added that this highlights the potential of the FinTech market in the continent.

In other words, improving the connectivity of the people living in Africa has meant there has been an opportunity to provide banking for the underbanked people by using modern technology. “This has been the most important driver for such FinTech movement because of the [market] opportunity,” argues Marconi, remarking that the adoption rate of services like the one offered by M-Pesa is much faster in Africa than in Europe and other parts of the world.

Albert Maasland, CEO of Crown Agents Bank, agrees. “The large unbanked population offers a huge and appealing opportunity for FinTech applications as there are very real problems that can be solved,” he says. “A population with little or no access to financial services but with high mobile penetration lends itself to rapid growth at low cost for FinTechs. Where Western banking and card based systems don’t cater to the problems that the unbanked in Africa face, many of the solutions are being built in the countries affected with an increasingly digitally literate and growing population. Investing in this localised development and FinTech ecosystem is very logical.”

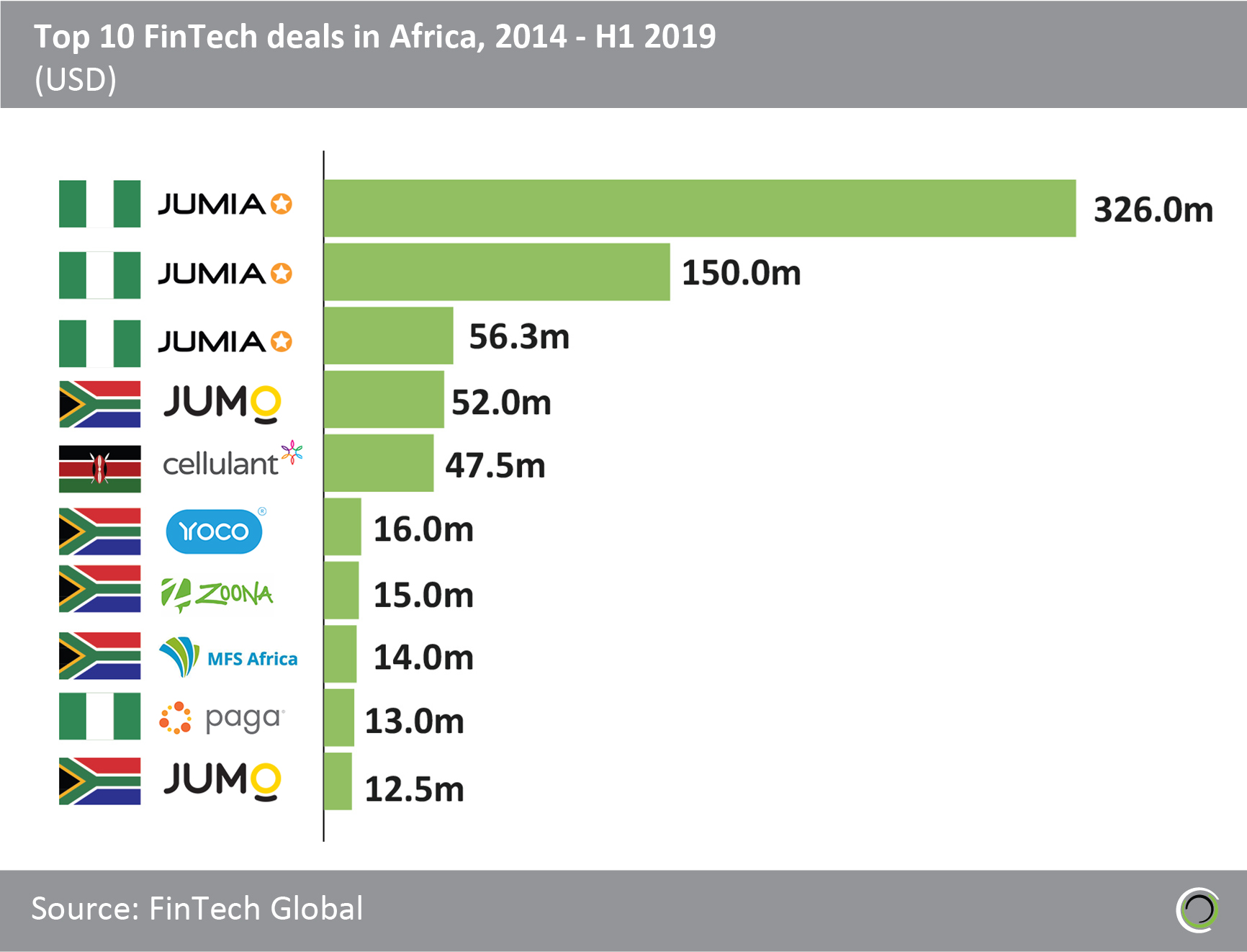

He argues that this is one of the reason why the lion’s share of the investment between 2014 and the beginning of 2019 was into payment and remittance companies with all top ten investment deals being in these sectors, according to FinTech Global’s own research. “When you have no access to financial services whatsoever, the first thing you need to be able to do is receive and move money,” Maasland explains. “Being able to make and receive payments is a core building block of financial services, so it’s not a surprise that this is where the bulk of investments are going given the high levels of previously unbanked populations.”

But that could just be the beginning. “What we will see more going forward will be so called add on services built on the core services provided by some of the leading FinTech firms as once you have the core infrastructure in place you can start building related services to meet additional customers’ needs,” suggests Marconi. “As an example we see some of the payment companies now moving into offering saving schemes, insurance, etcetera.”

So where will the African FinTech sector go next? If one would confer with EY’s report, the future could be optimistic. This sentiment comes from EY noting that the three main FinTech hubs – Kenya, Nigeria and South Africa – have all four essential factors needed to create thriving ecosystems. Although, the firm noted that there were some variations between the different countries.

Firstly, these three countries are seemingly brimming with talent and with few established opportunities available to them, many graduates are looking to start their own enterprises. Secondly, the continent is still significantly underbanked, meaning there’s a huge demand for these FinTech services. Thirdly, governments in these three countries are starting to show support for growing the sector. Finally, venture capitalists and others are showing a growing willingness to invest in the sector. “Trends in the [Sub-Saharan Africa] FinTech landscape are consistently moving in its favour; should they persist at the current rate, the sector could become an international contender in the near future,” the EY report stated.

Copyright © 2019 FinTech Global