Global InsurTech companies raised $6.21bn out of which United States accounted for more than $3.8bn

- Global InsurTech investment recorded its highest funding ever despite the coronavirus-caused economic uncertainty. InsurTech companies raised $6.2bn last year, a growth of 3.16% year-on-year compared to 2019. Interestingly, the rise in total funding was driven by deals below $50m which made up 33.5% of the total investment made in 2020 and recorded a growth of 19.5% from 2019 levels.

- Total capital invested grew at a CAGR of 38.4% from $1.7bn in 2016 to over $6.2bn at the end of last year. At the same time deal activity increased to 323 last year, a growth of 18.8% compared to 2019.

- Investment growth in the sector was supported due to demand that raised for on-demand insurance platforms amid the pandemic, which are helping the population have insurance coverage when they want and need to have it. Furthermore, the demand for digital access to insurance, faster, more personalised service and remote customer support increased the prospects of tech players in the industry.

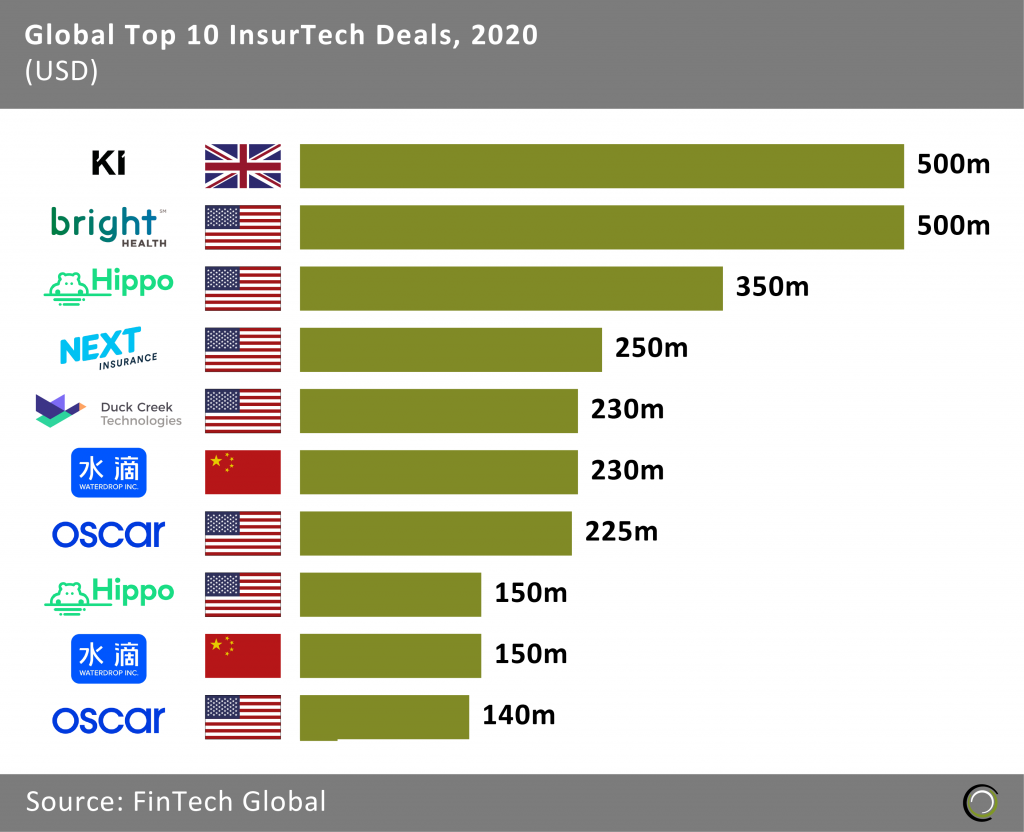

US companies raised seven of the top ten InsurTech deals globally in 2020

- The top ten InsurTech deals globally in 2020 raised in aggregate over $2.7bn making up 43.9% of the overall investment in the sector during the year.

- US companies took two out of the top three deals via Bright Health and Hippo Insurance. Bright Health, a health insurance service platform, raised a $500m Series E round led by Tiger Global Management, T. Rowe Price Associates and Blackstone Group. The funding was used to scale their transformative model and fulfil their purpose of lowering health care costs while improving outcomes, experiences and access.

- Hippo Insurance, an InsurTech company that uses technology to help homeowners maintain their properties, raised $350m in convertible notes. The funding will be used to support the company’s product rollout in additional states, to reach 95% of the US homeowners’ population in the next year, as well as providing additional capital for its insurance and reinsurance companies.

- The largest deal of the year was completed by Ki Insurance, the first fully digital and algorithmically driven Lloyd’s of London syndicate, which raised $500m in private equity from Blackstone Tactical Opportunities and Fairfax Financial Holdings. The funding will be used to rapidly scale the business and support their plan to provide a truly differentiated offering to brokers and clients.

- The largest deal outside the US and the UK was completed by Waterdrop, a Chinese online insurance technology platform that plans to solve the problem of high medical fees faced by many patients, which raised a $230m Series D round led by Tencent Holdings and Swiss Re group. The funding will be used to tap into artificial intelligence and big data for its products and services.

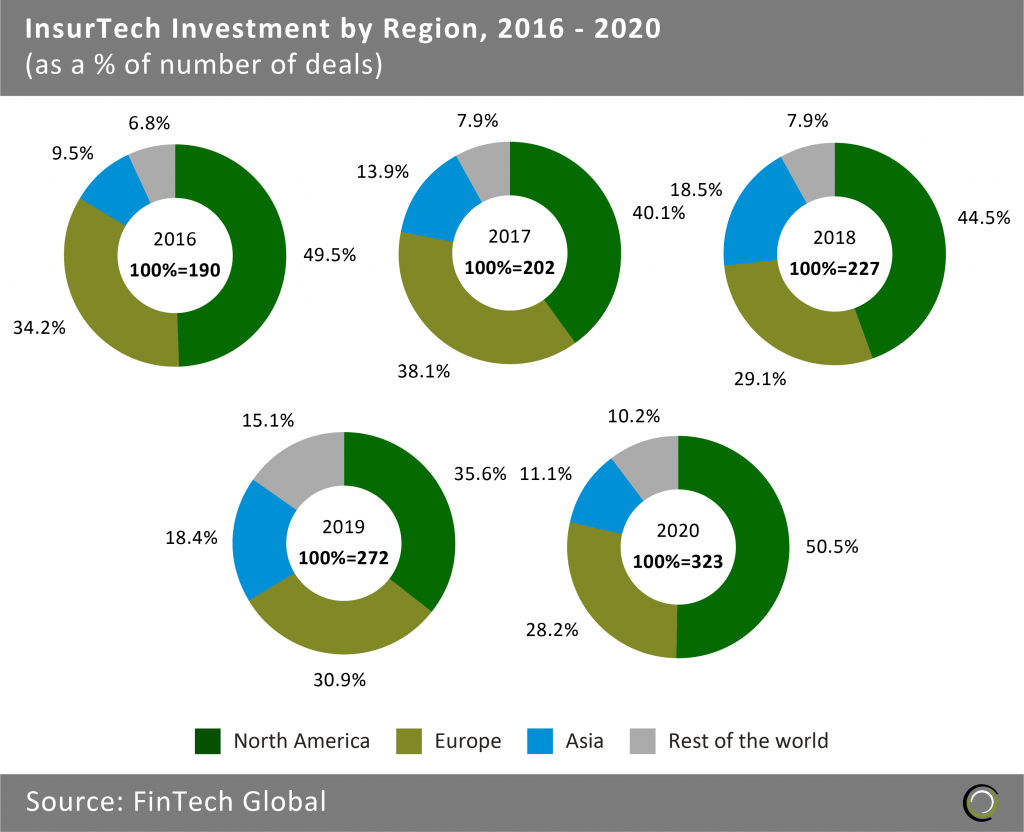

North American companies completed more than half of global InsurTech transactions in 2020

- North American InsurTech companies have seen a notable increasement in their global deal share since 2019, increasing 14.8 percentage points (pp) to 50.5% in 2020. This increase demonstrates a renewed interest in the region from investors given the rapid move to remote services. As such many companies needed new funding to either weather the pandemic or take advantage of new opportunities.

- While the North American share of deal activity increased, the Asian share of deal activity fell by 7.3 pp. The decrease in deal activity was due to the Covid-19 pandemic when the region had to lockdown to prevent the spread of the virus. Despite ending the lockdown in the region there has been a slower recovery in investments as foreign investors withdrew from the region amid political tension.

- European InsurTech companies despite having an increase in deal activity from 84 transactions completed in 2019 to 91 deals completed in 2020 also recorded a decrease in their share. It fell by 2.7 pp as investors shifted their focus to North American companies.

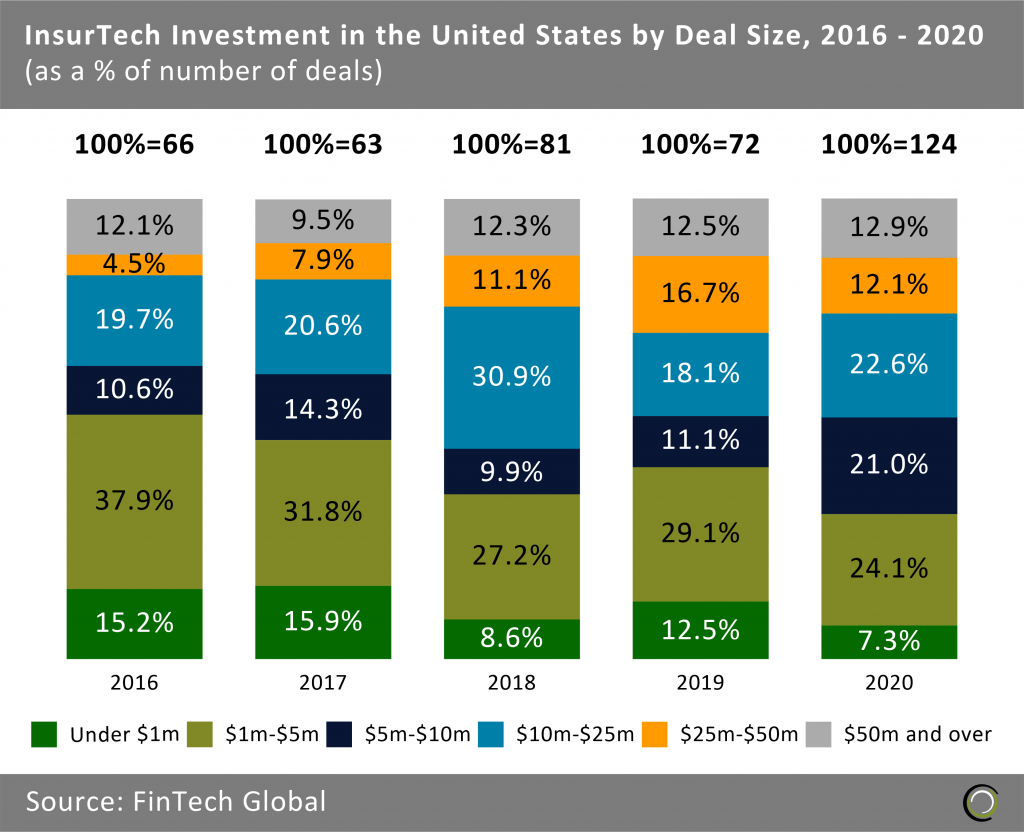

US deals between $5m-$10m see the biggest increase in 2020

- The share of early-stage deals under $1m, unsurprisingly, declined to 7.3% in 2020, its lowest level in five years. Investors shied away from riskier deals amid economic uncertainty and choose to place selective bets on newly formed companies.

- The share of deals valued between $5m and $10m increased 9.1 pp to 21%, the highest share in five years for the sector. The increase is driven by the Covid-19 pandemic as investors saw the growth opportunity in small to medium companies. Furthermore, investors supported companies in their portfolios with follow-on funding to preserve their capital and fund growth opportunities amid shifting prospects and opportunities.

- Deals of $50m and over saw an increase of 0.4 pp. Meaning that investors stayed on course with their investment strategy to support large companies and help them expand to other states and countries.

The data for this research was taken from the FinTech Global database. More in-depth data and analytics on investments and companies across all FinTech sectors and regions around the world are available to subscribers of FinTech Global. ©2021 FinTech Global