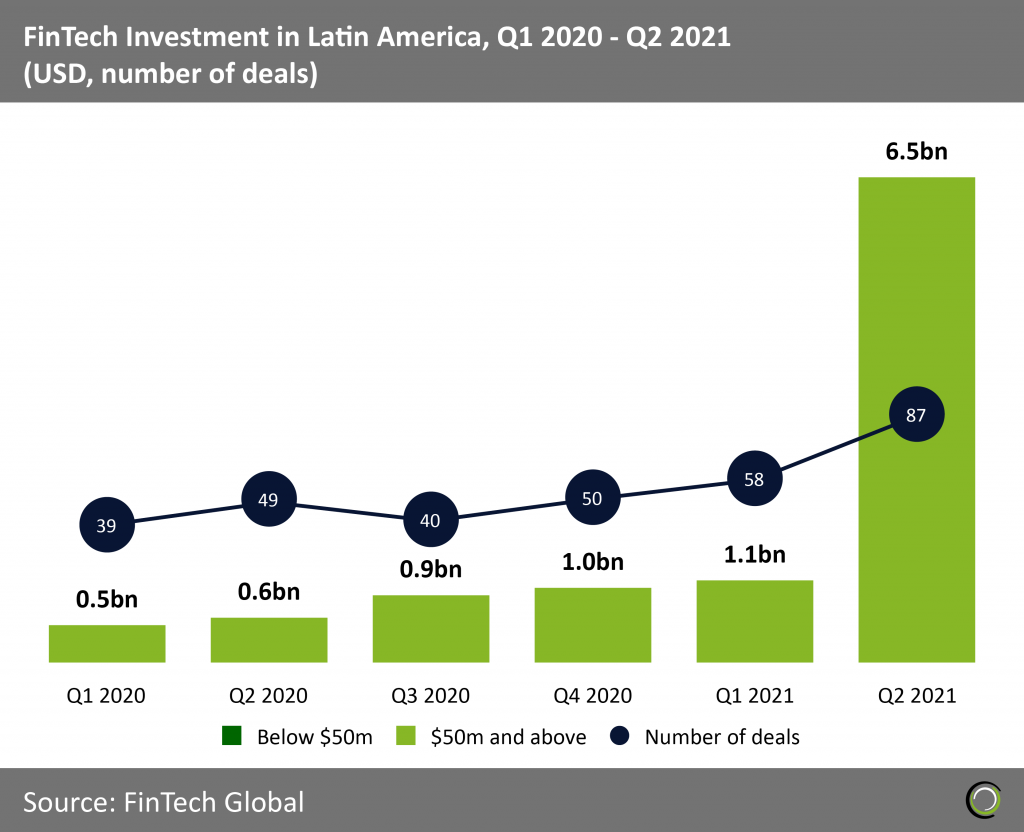

Funding in H1 2021 already surpassed last year’s total by $4.7bn, fueled by sizeable deals over $50m

- Latin American companies recorded huge growth in FinTech funding through the first half of 2021. Total capital invested at mid-year reached an all-time high of $7.6bn exceeding 2020’s total of $2.9bn. Funding has more than doubled compared to 2020 and is driven by sizable investments over $50m.

- Funding from deals $50m and above went up by $3.9bn in H1 2021 compared to 2020. The number of deals at mid-year is 145 and on track to exceed 2020’s deal count of 178. Funding under $50m is already ahead of 2020’s total just six months into the year with growth primarily powered by large, sizable transactions.

- The growth in Latin America’s FinTech adoption and demand can be attributed to the notoriously low adoption rates of financial services among consumers and Covid-19 induced acceleration for digital payments. These are setting the stage for FinTech players who are able to serve existing customers better and introduce new underbanked segment of the population to the financial system for the first time

Investment in Q2 is the principal driver of Latin America’s funding growth in 2021

FinTech companies in Latin America raised 50% more deals in the second quarter compared to Q1 2021. Q2 is the prime contributor to the exponential growth seen in the first half of the year with companies raising $6.5bn over 87 deals versus $1.1bn over 58 deals in the first three months of 2021. Out of Q2 2021’s total funding, 31% came from a massive $2.1bn funding round by C6 Bank, a company offering full-service digital banking services to individuals and businesses.

FinTech companies in Latin America raised 50% more deals in the second quarter compared to Q1 2021. Q2 is the prime contributor to the exponential growth seen in the first half of the year with companies raising $6.5bn over 87 deals versus $1.1bn over 58 deals in the first three months of 2021. Out of Q2 2021’s total funding, 31% came from a massive $2.1bn funding round by C6 Bank, a company offering full-service digital banking services to individuals and businesses. - Latin America’s FinTech investment growth is highlighted by the drastic jump in investments in Q2 2021. After the small dip in number of deals in Q3 2020, deals counts are trending upward with the most deals raised in Q2 2021. Investments have risen steadily between Q1 2020 and Q1 2021 leading to the big jump in investments in Q2 2021.

- Funding levels are 6x times higher in comparison to Q1 2021 and the highest ever raised in the Latin American FinTech sector. The boost in investments can be attributed to the increasing demand from consumers and businesses for digital payment solutions. With Covid-19 having a profound impact in the FinTech landscape, Latin America’s cash-based economy witnessed spurring innovation out of necessity. With businesses shutting down, digital banking and online payments became a necessity for continued operation, and this accelerated FinTech adoption that would otherwise have taken many years.

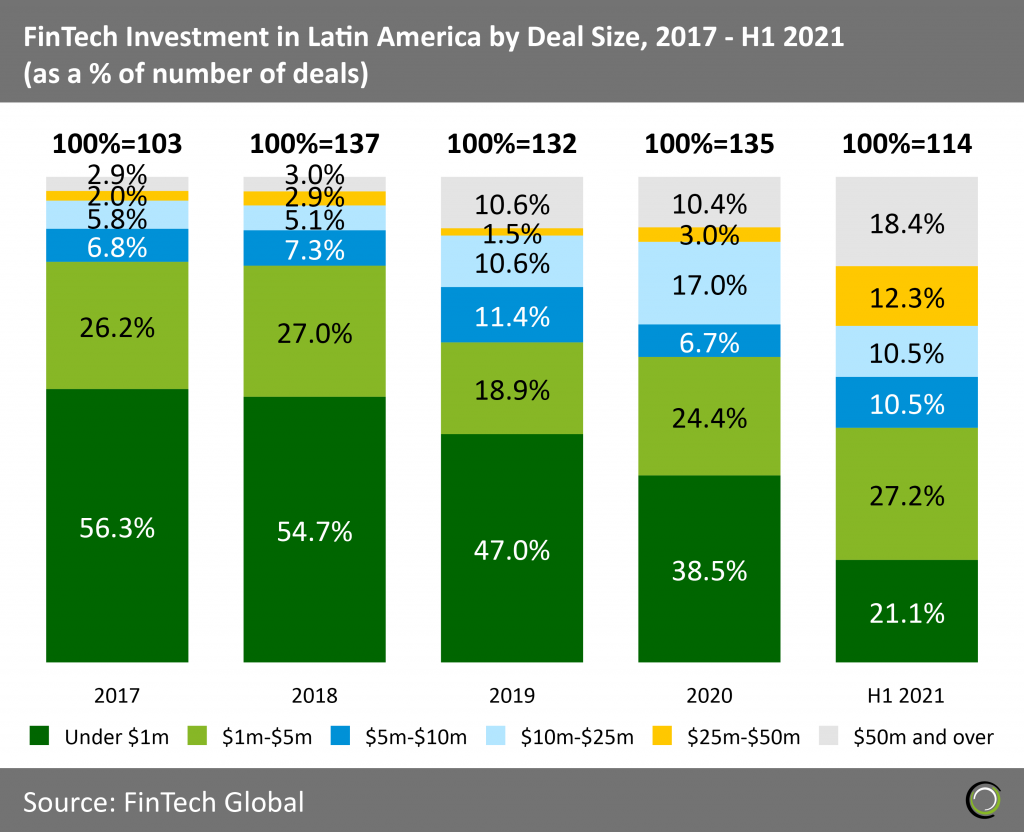

Sizable investments above $25m are seeing a spike in 2021 signaling investors’ interest in well-established companies

The share of deals $25m and above reached an all-time high in the first half of 2021. The share of deals in the $25m – $50m size bracket has grown by 9.3 percentage points over 2020’s share of deals. Deals $50m and above have increased by 8 percentage points in comparison to 2020. Deal sizes reveal investors showing an increasing appetite in sustaining seed-stage investments that are maturing and demanding more funding.

The share of deals $25m and above reached an all-time high in the first half of 2021. The share of deals in the $25m – $50m size bracket has grown by 9.3 percentage points over 2020’s share of deals. Deals $50m and above have increased by 8 percentage points in comparison to 2020. Deal sizes reveal investors showing an increasing appetite in sustaining seed-stage investments that are maturing and demanding more funding. - The share of deals under $1m continued to drop from 56.3% in 2017 to 21.1% in H1 2021. The shift to sizeable investments shows investors’ interest in well-established maturing companies that are tapping into new FinTech innovations capable of disrupting current technologies.

- Deals in the $1m – $5m size bracket are at 27.2%, the highest deal size bracket in H1 2021. Deals in this category are seeing a reemergence after the dip in 2019. The accelerated adoption of FinTech caused by Covid-19 in Latin America has investors and businesses in search of new technologies that can serve the growing demand from consumers and hence a mix of both small and large funding can be seen in H1 2021.

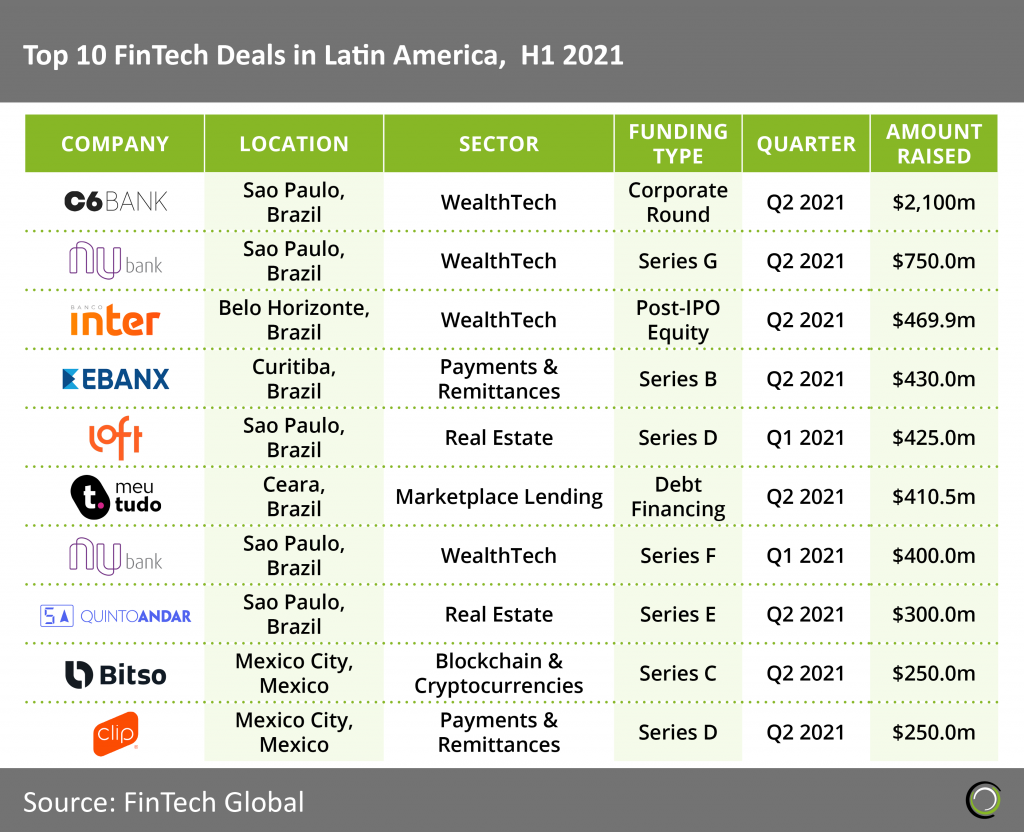

C6 Bank’s enormous $2.1bn funding is the leading Latin American investment in H1 2021 followed by challenger Nubank

Eight out of the top ten FinTech deals in Latin America were raised in the second quarter of 2021. As previously mentioned C6 Bank topped the list with $2.1bn funding round raised from a group of 40 private investors. The capital raised is deemed to be invested to increase customer base, expand investment platform, and develop new business lines. The company’s 4m clients are a far cry from its challenger, Nubank.

Eight out of the top ten FinTech deals in Latin America were raised in the second quarter of 2021. As previously mentioned C6 Bank topped the list with $2.1bn funding round raised from a group of 40 private investors. The capital raised is deemed to be invested to increase customer base, expand investment platform, and develop new business lines. The company’s 4m clients are a far cry from its challenger, Nubank. - Nubank, a leading financial technology company and largest independent neo bank in the world, claims to have 40m customers. Nubank raised two funding rounds this year at $750m and $400m in the first and second quarters respectively. Nubank’s $750m funding is part of series G fundraising with Warren Buffett’s Berkshire Hathaway Inc. investing $500m. The company is said to be listed on the US stock exchange this year.

- Four of the top 10 deals were raised by neo banking services corresponding to the boom in neo banks and digital wallets currently taking place in Latin America. There is a large latent demand for FinTech in Latin America. This is mainly due to the majority of customers being underbanked or unbanked. Systemic reasons behind the low adoption rates are mainly due to banks biased services to affluent and highly cash-based paper payments.

- Furthermore, Brazil is home to eight of the top 10 FinTech deals. Brazil is leading the Latin American FinTech landscape with 41% of all deals completed between 2017 and H1 2021. Smartphones are broadly adopted in Brazil than in any other Latin American country. This combined with the severe lack of banking services has led the country leading Fintech in Latin America.

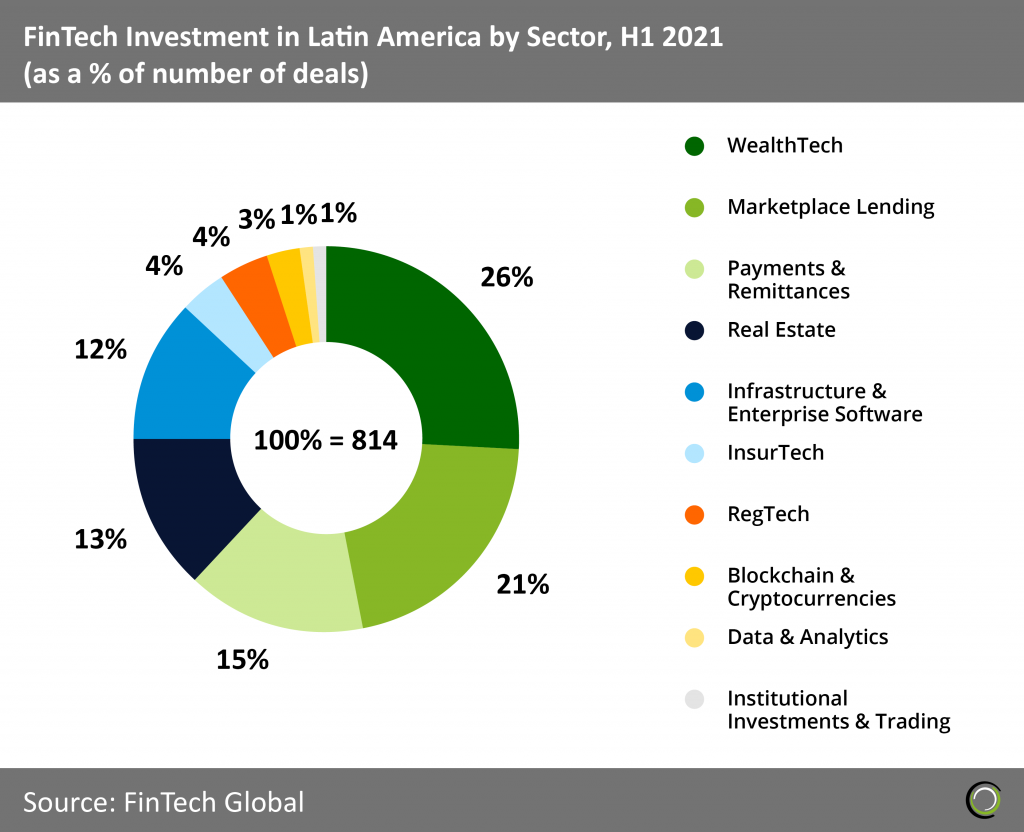

WealthTech companies hold the top spot for deal activity in 2021 as Latin American FinTech investments are setting records

WealthTech is the leading FinTech sector in Latin America with 26% deals completed in H1 2021. With a high percentage of population under 25 years, consumers in the region expect banking services to mirror consumer apps. Digital banks are meeting this expectation and are breaking traditional banking barriers that only served the affluent Latin American demographic. Investment practices once considered accessible only to the wealthy population are gaining momentum with the rise of robo-advisors pushing consumers to think beyond their savings account.

WealthTech is the leading FinTech sector in Latin America with 26% deals completed in H1 2021. With a high percentage of population under 25 years, consumers in the region expect banking services to mirror consumer apps. Digital banks are meeting this expectation and are breaking traditional banking barriers that only served the affluent Latin American demographic. Investment practices once considered accessible only to the wealthy population are gaining momentum with the rise of robo-advisors pushing consumers to think beyond their savings account. - Marketplace Lending companies hold 21% of deal activity this year. The severe banking crisis and heated economy has led to a huge latent credit demand, both from individuals and SMEs. Additionally, high unsecured overdraft payments, credit card fees, and high borrowing costs from banks has shifted consumer demands to more affordable and easy lending platforms.

- Payments and Remittances came in third taking 15% of deal activity this year. FinTech friendly regulations such as the “Ley Fintech” have given the power to FinTech companies to operate under the same regulatory framework as traditional banks. Regulations such as these around mobile payments and digital wallets have provided a helping hand for as companied such as Ebanx, an all-in-one payments solution to businesses.

- RegTech constitutes 4% of the FinTech sector in Latin America. As more neo banks and digital wallets become prominent, the need for regulations from authorities and compliance specifications will only demand more innovation and use of technologies for compliant onboarding, transaction monitoring and risk management.

The data for this research was taken from the FinTech Global database. More in-depth data and analytics on investments and companies across all FinTech sectors and regions around the world are available to subscribers of FinTech Global. ©2021 FinTech Global