Funding in the first three quarters already surpassed 2020 levels by $10.5bn, driven by a higher number of large deals.

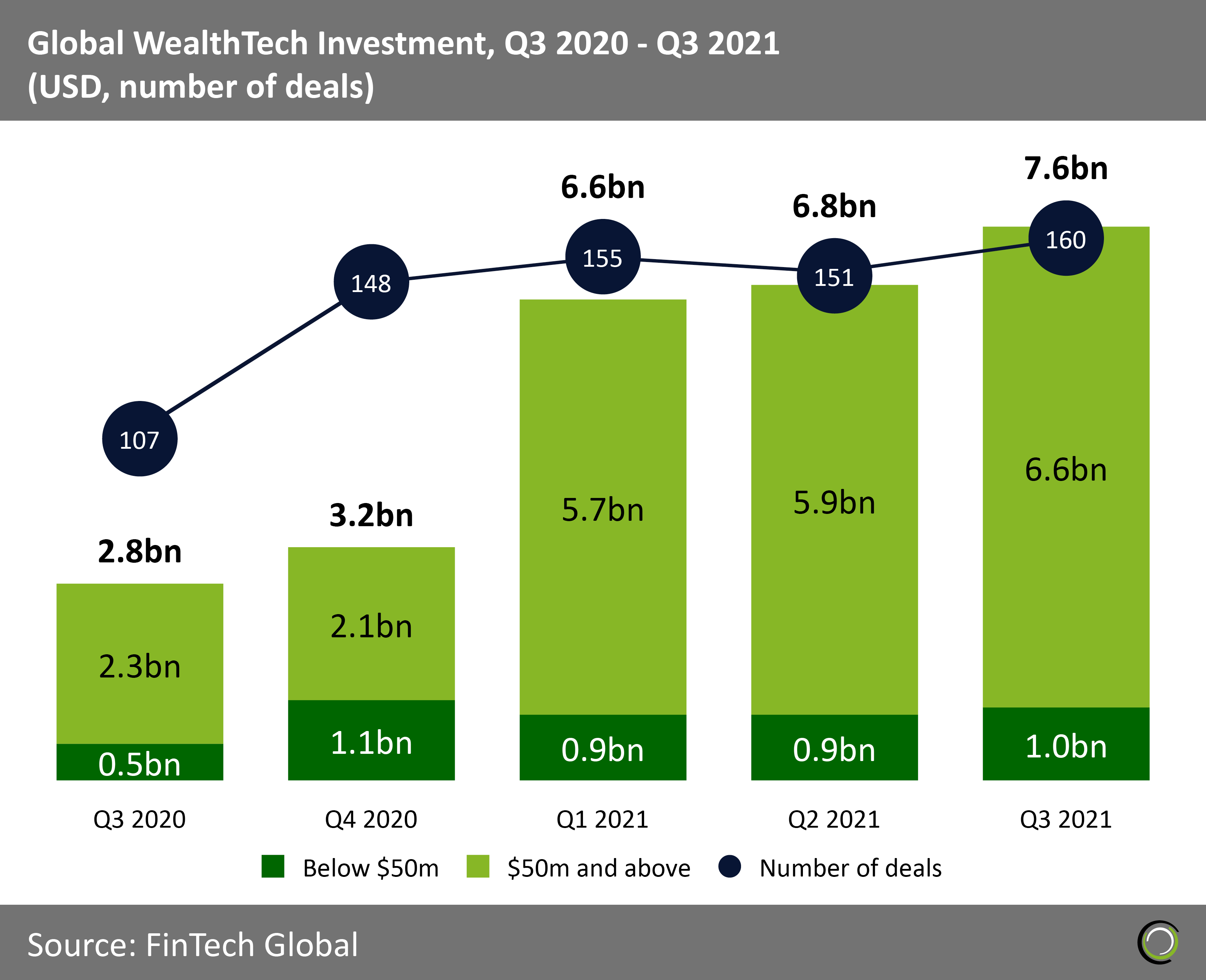

- Following the strong investment numbers in the WealthTech sector discussed in our July 2021 research, Q3 2021 is seeing even a stronger performance. Deal activity reached 446 transactions so far this year while total capital invested hit $20.9bn, a new annual record. Q3 2021 was the largest quarter ever for number of funding deals recorded (160) and total funding raised ($7.6bn). Among these, 64 deals were signed by Online Banking companies and 35 by Retail Investing & Trading startups as demand for this services post pandemic continues to grow.

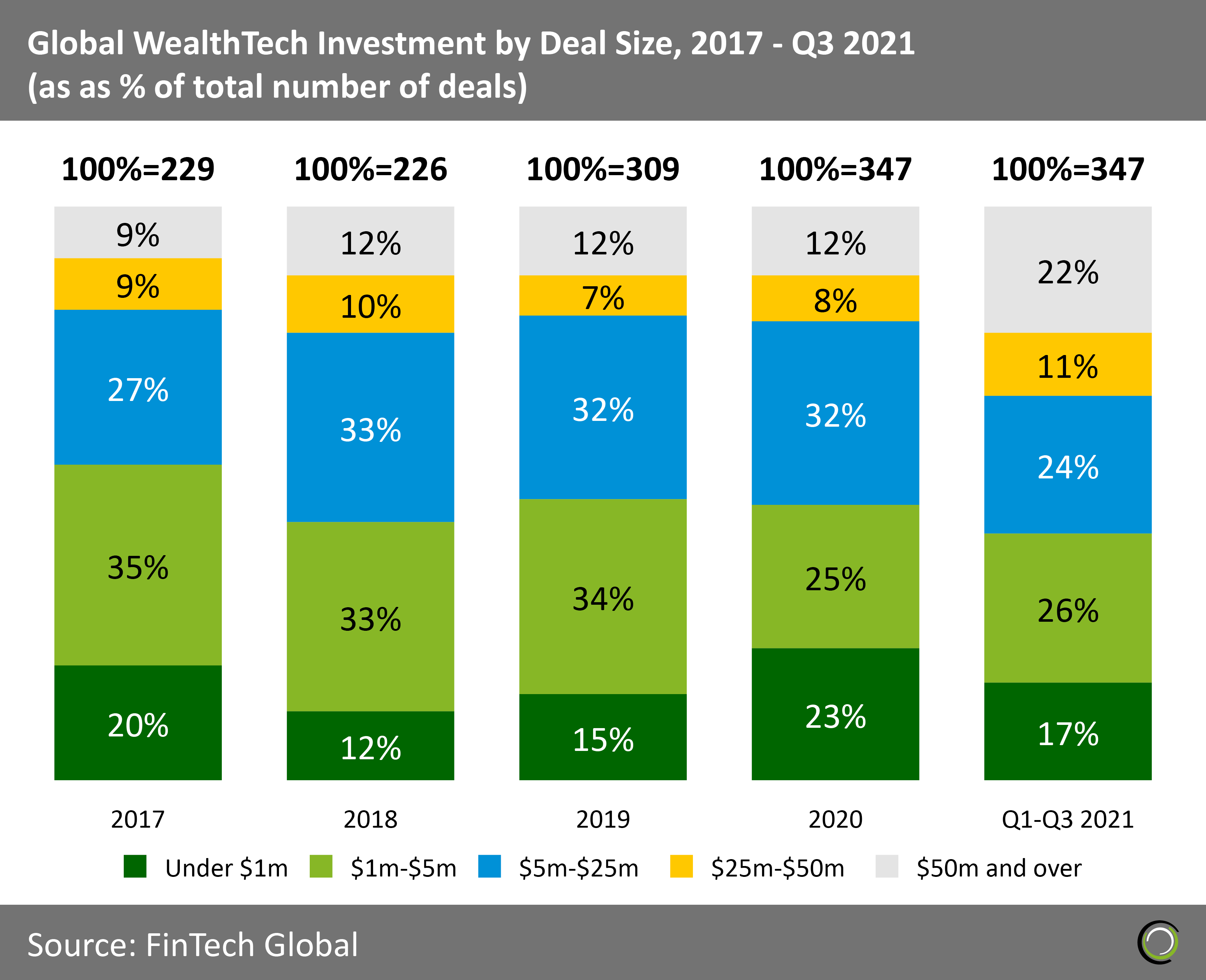

- Deals under $50m are still growing in 2021, but not as much as deals equal and over $50m which went from $6.7bn in 2020 to $18.1bn during the first nine months of 2021. While funding per deal has remained stable between 2018 and 2020 with an average funding of $27m per deal, in 2021 we are seeing a doubling with an average of $56.9m per funding round.

- Between 2017 and 2018, the number of deals in the WealthTech sector did not increase much. Digital platforms for wealth management were niche solutions. In 2019, the first sign of a change appeared with the advent of Robinhood – a stock trading platform that allows everyone to buy and sell stocks with zero commission. After the Covid-19, digital adoption expanded especially in Wealth Management. The pandemic acted as an accelerator for WealthTech, with the younger generations jumping on the bandwagon to get involved. From 2019 to Q3 2021, the number of deals increased exponentially reaching a new high this year with a 24% increase from 2019 levels.

The sector recorded huge jump in funding from deals $50m and above since the start of the year

A major indicator of the growth in WealthTech investments is highlighted by the big jump in funding from deals equal and above $50m since Q1 2021. From $2.1bn in Q4 2020, the WealthTech sector reached $5.6bn in capital raised from deals in the size bracket in Q1 2021. Funding has doubled for the levels recorded in Q4 2020 since then, keeping numbers strong in both Q2 and Q3 2021.

A major indicator of the growth in WealthTech investments is highlighted by the big jump in funding from deals equal and above $50m since Q1 2021. From $2.1bn in Q4 2020, the WealthTech sector reached $5.6bn in capital raised from deals in the size bracket in Q1 2021. Funding has doubled for the levels recorded in Q4 2020 since then, keeping numbers strong in both Q2 and Q3 2021.- Resources and infrastructures like digital platforms and services were a major necessity to cope with since the changes brought by the pandemic. The turning point was in Q1 2021, but we could have seen the first signs of digital innovation in Q2 2020 when WealthTech responded to the necessities of the market. Companies started using technology to improve efficiencies and evolve their business by hyper personalise their product and services offered to the mass market.

- In 2020, the amount of funding from deals under $50m remained constant over time except for Q4 2020, which experienced a growth of 116% compared to Q3 2020. This increase in funding is matched with a 38% rise in overall deal activity from Q3 to Q4 2020.

The share of deals under $25m collapsed in 2021, pointing out that investors back later stage companies

As of Q3 2021, the number of deals with disclosed value in 2021 already reached 2020’s levels, with a total of 347 deals in the Global WealthTech sector. Nevertheless, the average funding per deal doubled from 2020 to Q3 2021, going from $26.6m in 2020 to $56.9m in 2021. The number of deals has increased throughout the three quarters of 2021, recording 114 public reported deals in Q1 2021, 123 in Q2 2021 and 130 in Q3 2021.

As of Q3 2021, the number of deals with disclosed value in 2021 already reached 2020’s levels, with a total of 347 deals in the Global WealthTech sector. Nevertheless, the average funding per deal doubled from 2020 to Q3 2021, going from $26.6m in 2020 to $56.9m in 2021. The number of deals has increased throughout the three quarters of 2021, recording 114 public reported deals in Q1 2021, 123 in Q2 2021 and 130 in Q3 2021.- Covid-19 accelerated the shift towards digital adoption of WealthTech services, speeding up trends that we already taking place in the sector. Millennials and Gen Z are more and more interested and engaged in how to manage their finance, where and in what place to put their savings ins. In addition, older generations had to adopt WealthTech in order to cope with the shift in users’ behaviour and social distancing during the pandemic.

- Since the share of deals equal and above $25m is getting bigger and bigger (we can see an increase by 13 percentage points (pp) from 2020 to Q3 2021), we can deduce that more and more capital is moving into matured WealthTech companies. To adapt to the changing technological environment, well established companies need more funding for investing in AI, Big Data or other technologies. Among the mega-deals in 2021, Robinhood recorded the two largest during Q1 2021 amounting for a total of $3.4bn.

- Mega rounds (rounds above $50m) are growing in 2021, recording 9pp increase from 2020. 79 are the companies that managed to raise more than $50m per funding round – mainly via Ventures and debt financing. These mega funding rounds were led by Online Banking and Retail Trading and Investing, in need for more capital to support the acquisition of a larger customer basis. Only one IPO was registered in a round of $471m for Banco Inter (an online banking service established in Brazil) by Stone Pagamentos SA.

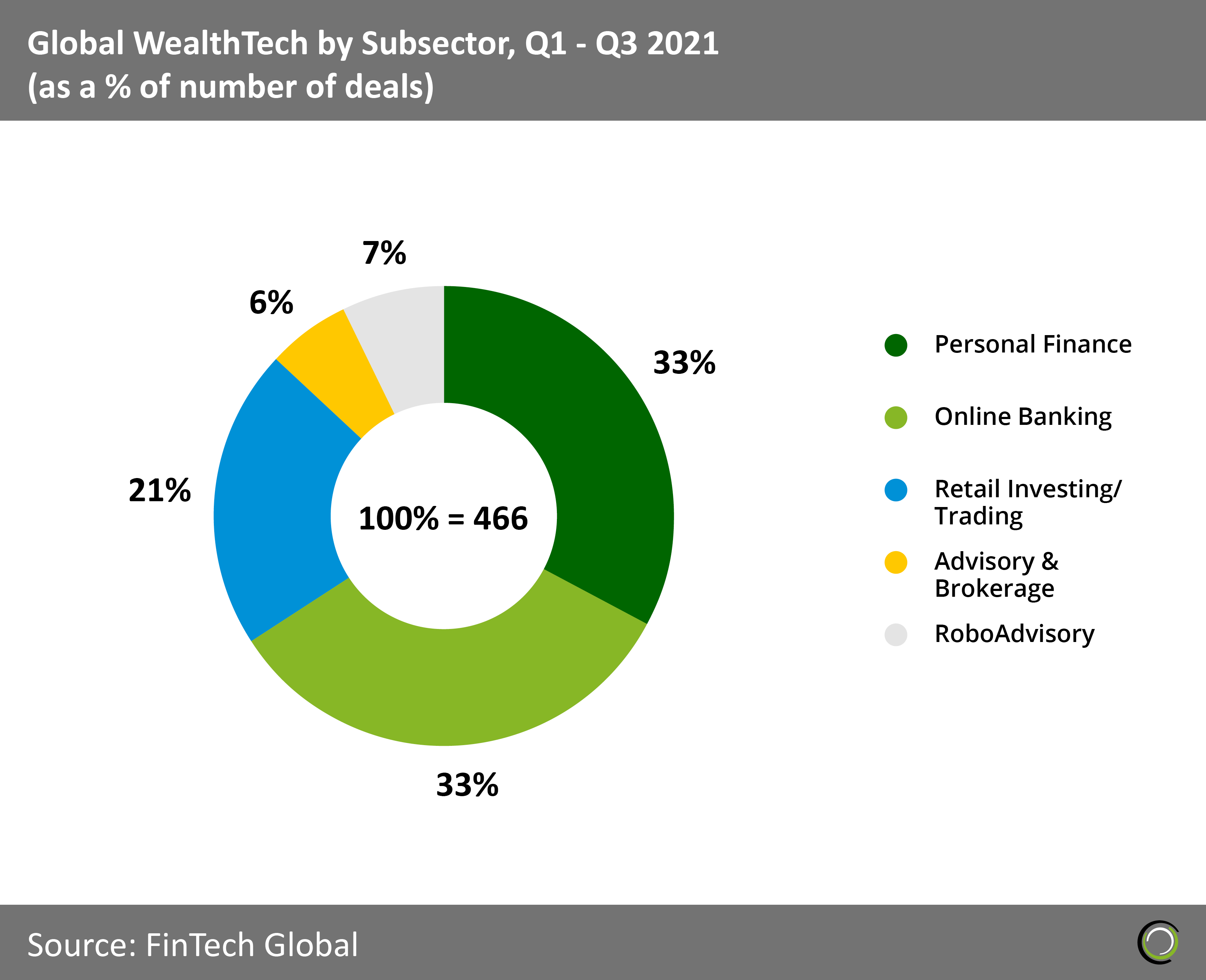

Online Banking gained popularity especially among Gen Z, holding 33% of total Global WealthTech deals in 2021.

With the creation of finance and investing apps over the past 15 years, WealthTech has gained ground among the other FinTech sectors. Leading in 2021 are Personal Finance and Online Banking, collecting 66% of all deals. Especially among Millennials and Gen Z, Online Banking has become essential in their lives since it does not require long and standardised procedures. Mainly used for budgeting, checking credit scores and creating savings goals, mobile banking apps are a good (but yet not perfect) solution for those people that do not see the necessity to have a human assistance by their bank representative. – impact of Covid, also budgeting tools for millennials are key when they are not earning much

With the creation of finance and investing apps over the past 15 years, WealthTech has gained ground among the other FinTech sectors. Leading in 2021 are Personal Finance and Online Banking, collecting 66% of all deals. Especially among Millennials and Gen Z, Online Banking has become essential in their lives since it does not require long and standardised procedures. Mainly used for budgeting, checking credit scores and creating savings goals, mobile banking apps are a good (but yet not perfect) solution for those people that do not see the necessity to have a human assistance by their bank representative. – impact of Covid, also budgeting tools for millennials are key when they are not earning much- With the use of AI and Machine Learning, banks are able to provide value-added services and personalise their services for the needs of each customer. Neo and major banks can understand the new generation of clients and fulfil its demands. Digital banks are becoming more and more popular since they are able to meet the needs of tech-savvy consumers. They are intuitive and easy-to-use services, and they require just few steps for you to create an account. A digital-first philosophy will help these banks reach the projected $471bn market size by 2027, running the banking sector. However, traditional banks have to respond in order to keep up with their rivals: via third-party providers and the adoption of digital services and offerings, traditional banks are slowly growing and becoming the next competitors in the online banking market.

- When Covid-19 exploded, armchair trading became an extremely popular hobby among everyday people, counting Robinhood as leader. Registering 97 deals out of 210 from Q1 to Q3 2021, Retail Investing and Trading is giving the possibility to platforms and app users to invest for themselves in a fast and easy way, and with small commissions. However, two important aspects must be looked at in the future: the changes in the regulatory system and rules, and the gamification of investing inside these platforms.

- Now more than ever, there is a strong attention on the environment. Wealth Tech companies and investors have to consider more carefully environmental, social and corporate governance (ESG) factors. This is what clients nowadays are looking at, along with gender equality (hot topic right now as highlighted by the NORC survey made by the Univiersity of Chicago in June 2021), racial equality, and LGBTQ+.

- As the pandemic brough the necessity to digitalise as many services as possible, Robo Advisory is gaining ground in the WealthTech world, with 34 deals recorded in 2021. Millennials are those who have changed their investment habits the most and relied more on Robo Advisers. However, the gap between Millennials and older generations widened even more since the latter group is still intimidated by automated services without a physical professional guidance. Robo Advisors’ lack of emotional guidance and complete ad hoc personalisation is a big barrier for more professional figures, usually investing large amount of money.

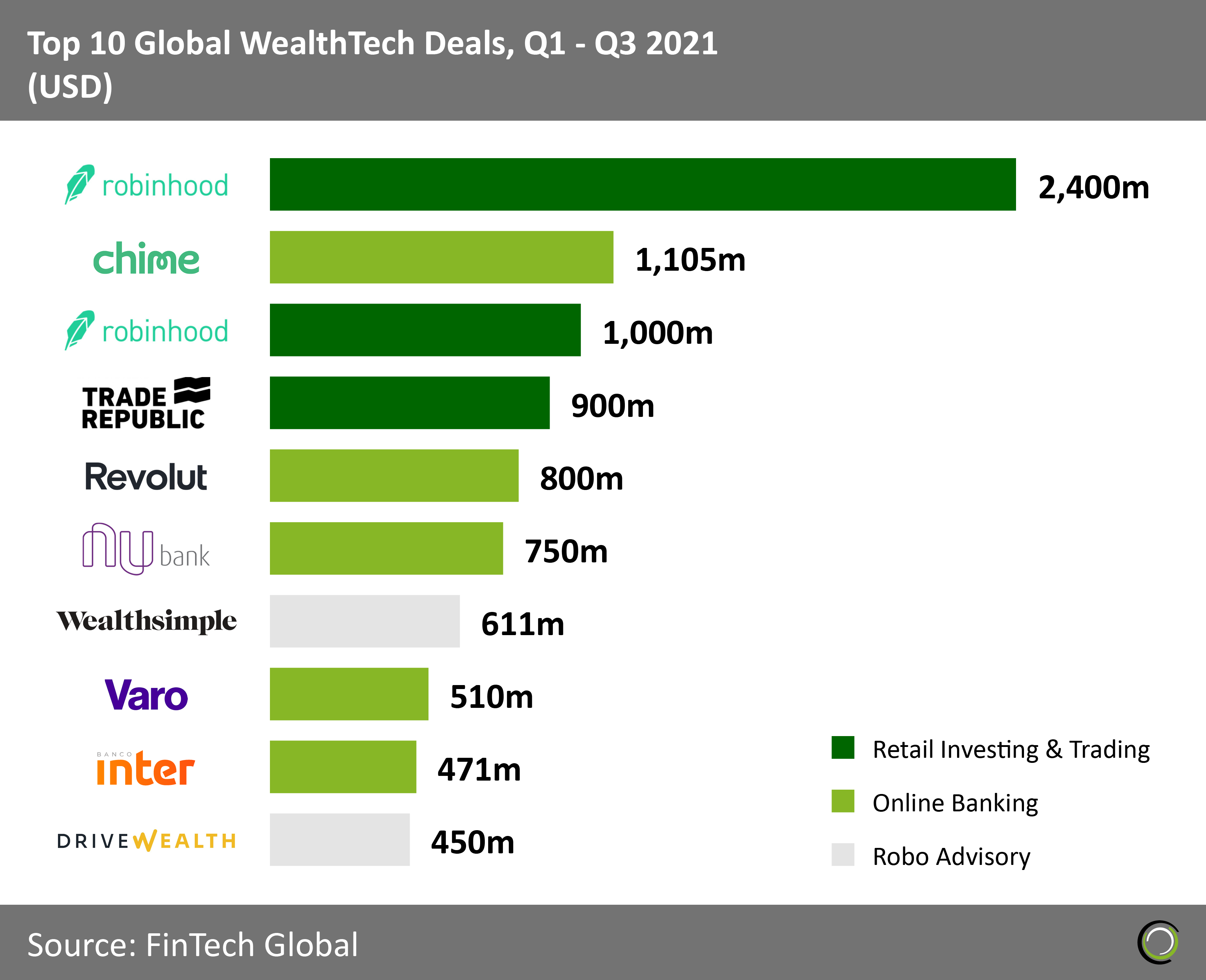

As of Q3 2021, Robinhood still Leads 2021’s Top Ten Deals.

Five out of the top ten deals were signed by digital banks, collecting $3.6bn. Among those, the largest deal came from Chime, a fee-free online bank with headquarter in San Francisco, California, that helps its clients with savings and financial decisions. The company needed funds to invest in scaling operations and lunch new products and services. It has managed to get $1.1bn via a Series G funding from Dragoneer Investment Group, General Atlantic, Sequoia Capital Global Equities, SoftBank Vision Fund and Tiger Global Management.

Five out of the top ten deals were signed by digital banks, collecting $3.6bn. Among those, the largest deal came from Chime, a fee-free online bank with headquarter in San Francisco, California, that helps its clients with savings and financial decisions. The company needed funds to invest in scaling operations and lunch new products and services. It has managed to get $1.1bn via a Series G funding from Dragoneer Investment Group, General Atlantic, Sequoia Capital Global Equities, SoftBank Vision Fund and Tiger Global Management.- As mentioned above, Robinhood detains the top (and not only) position thanks to a funding round of $2.4bn via a convertible note from seven investors, among which 9Yards Capital and Sequoia Capital. This funding round followed the one happened just three days before due to a high demand for cash. The reason behind this shortage of cash was the relatively high trading traffic happening between January and February 2021. In the last weeks of January, the expected amount Robinhood should have posted increased tenfold for stocks like GameStop’s. After a first round of $1bn by VC investors, Robinhood needed a fill up to meet the regulatory requirements.

- Two Robo Advisory companies are among the top ten deals of 2021. Wealthsimple, a Canadian financial tools provider for investor growth and money managing, managed to raise $610.8m in May 2021, $160.7m more than the other Robo Advisory company on the list, DriveWealth – a cloud-based, API-driven brokerage infrastructure developer based in the United States.