Capital invested in Australasian FinTech companies surpassed $750m across 56 deals last year

- Between 2015 and 2016, total FinTech investment in Australasia fell by more than half. This was mainly due to the absence of large deals valued above $100m. However, even when large deals are excluded from the analysis, funding from sub-$100m transactions also decreased by 7.5%.

- Investment subsequently rocketed in 2017 to reach $753.5m. This was fuelled by the return of deals over $100m, while funding from sub-$100m deals also doubled. Overall, compared to 2016 total funding more than trebled.

- Despite the fluctuations in capital invested since 2015, deal activity has remained steady over the same period. As a result, the average deal size jumped from $4.4m in 2016 to $15.4m in 2017.

- FinTech investment data in Australasia consists exclusively of deals to companies based in either Australia or New Zealand. Governments in both countries have taken steps to support the growing FinTech sector in recent years. For example, the Australian government announced the extension of its FinTech regulatory sandbox in the 2017-18 Budget, in addition to removing the double taxation of digital currency and easing restrictions on crowdfunding.

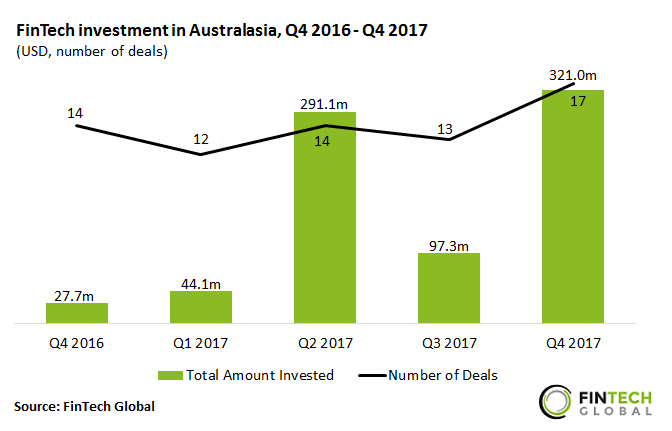

Investment in Australasian FinTech companies bounced back in Q4 2017 to set a record

- The second and fourth quarters last year are the top two funding quarters in the region to date. Q4 was the strongest of these in terms of capital invested with a total of $321m, a YoY increase of 11.6x. This follows a quieter Q3 when just $97.3m was invested, a historically mid-range value.

- The largest deal in Q4 2017 was a $91.5m debt financing round in MoneyMe, a consumer lending platform. The transaction was led by Fortress Investment Group with co-investment from Evans & Partners.

- Deal activity also increased in the final three months of last year to reach 17 deals, the highest deal activity level over the last five quarters

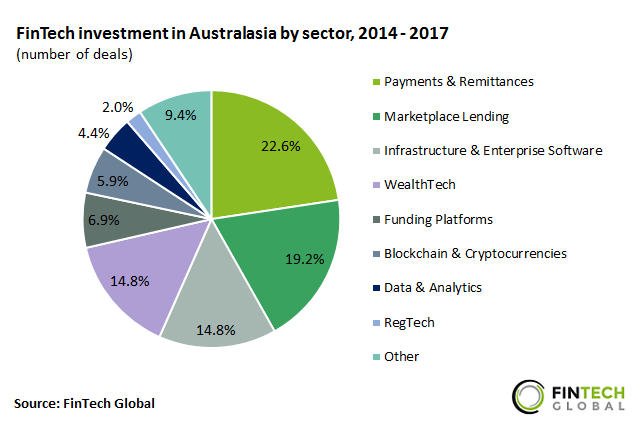

Australasian FinTech companies that specialise in Payments & Remittances received nearly a quarter of all deals

- Payments & Remittances companies received the highest share of deals between 2014 and 2017 with 22.6%. The largest deal in this category over that period was a $72m investment in Sydney-based Tyro Payments, a provider of payment systems for businesses. The venture round was led by Tiger Global Management with co-investment from TDM Asset Management.

- Marketplace Lending and Infrastructure & Enterprise Software followed as the next top sectors in terms of deal activity, with a 19.2% and 14.8% share of all deals, respectively.

- A further quarter of deals went to companies offering solutions in WealthTech, Funding Platforms and Blockchain & Cryptocurrencies. The most notable funding round in this category was a $53m ICO raised by Melbourne-based Hcash, a blockchain security startup, in Q4 2017.

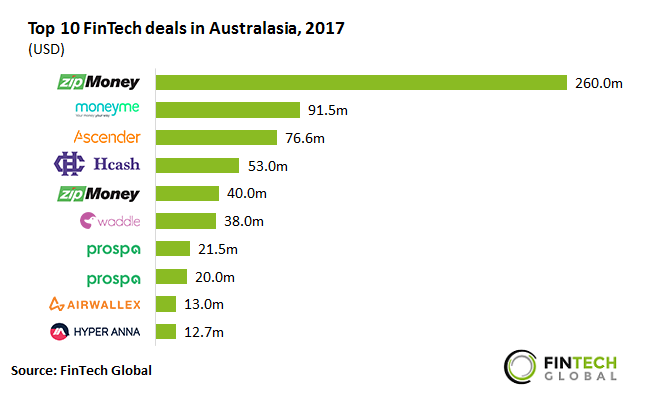

The top ten FinTech deals in Australasia accounted for nearly 85% of last year’s total funding

- The top ten Australasian FinTech deals in 2017 raised a combined total of $626.3m which equates to 83.1% of the total funding for the year.

- zipMoney Payments, a digital credit card for online shopping, raised the largest deal in 2017. The company received a $260m debt facility led by National Australia Bank in Q2. This was followed by a strategic investment of $40m by Westpac in third quarter of 2017.

- Prospa, an online SME lender, also had two deals in the top ten. The company raised $21.5 in a Series B round led by Entrée Capital and AirTree Ventures, before receiving $20m in debt financing from Partners for Growth in Q4.

- All top ten investments last year were raised by companies based in Australia; seven are headquartered in Sydney and three in Melbourne.

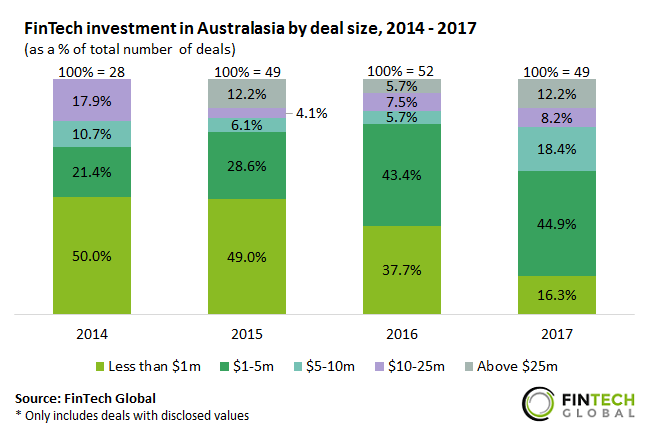

There was a further shift towards larger deals last year as the industry continued to mature

- The share of deals valued below $1m dropped by 11.3 percentage points (pp) between 2015 and 2016. This fell a further 21.4pp last year when sub-$1m deals accounted for just 16.3% of all investments.

- From 2015 to 2016, the fall in smaller deals was mainly offset by deals valued between $1-5m which increased in share from 28.6% to 43.4%.

- The further decline in small deals in 2017 was taken up by even larger deals valued between $5-10m and above $25m, which increased in share by 12.7pp and 6.5pp, respectively.