The loss of momentum in global InsurTech investment after 2015 was simply due to the volatility of large deals

- 2015 was a record year for global InsurTech investment with over $2bn-worth of funding. This was due to a $937m investment in Shanghai-based ZhongAn, a digital insurance provider. The company raised the funding in a Series A round from Morgan Stanley, CICC and CDH investments.

- Total InsurTech funding remains variable due to the irregularity of larger deals. However, funding raised from deals valued below $100m has increased steadily every year since 2014 at a CAGR of 21.8%.

- Similarly, if the previously mentioned ZhongAn deal in 2015 is excluded then total investment also increased consistently year on year since 2014.

- Despite the increase in total funding last year, deal activity declined by 6.3% compared to 2016.

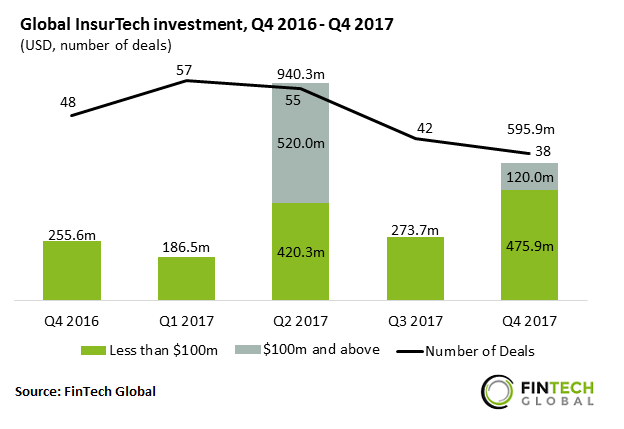

Deal activity slowed down in the second half of 2017

- Q2 2017 was the second strongest funding quarter for global InsurTech companies to date with $940.3m invested across 55 deals. Three deals valued over $100m were closed during this quarter including the largest of the year, a $230m investment in London-based Gryphon Insurance. The life insurance platform raised the funding in a private equity round led by Punter Southall Group and Leadenhall Capital Partners.

- The final quarter of last year saw a total of $595.9m invested which makes it the fourth strongest funding quarter to date.

- The largest deal of Q4 2017 was a $120m investment in Lemonade, an InsurTech focusing on home and renter’s insurance. The Series C round was led by Softbank with co-investment from Sequoia Capital and General Catalyst, among others.

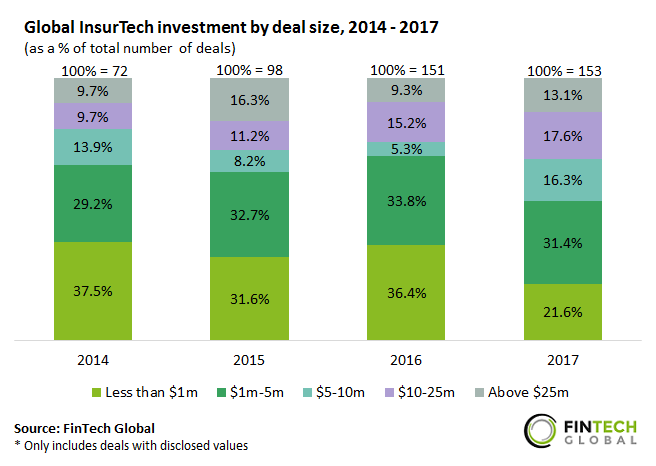

There was a clear shift towards larger deals in 2017

- Between 2014 and 2016, there was no clear trend towards larger deals. Although deals valued below $1m decreased in share by 5.9 percentage points (pp) in 2015, this value then increased in 2016 to regain most of its original share.

- Similarly, large deals valued above $25m almost doubled in share between 2014 and 2015, from 9.7% to 16.3%. However, the category’s share then decreased to 9.3% in 2016.

- The most significant shift towards larger deals took place in 2017. Sub-$1m deals dropped in share from 36.4% in 2016 to 21.6%. This fall was mainly offset by deals valued between $5-10m which more than tripled in share from 5.3% to 16.3% over the same period.

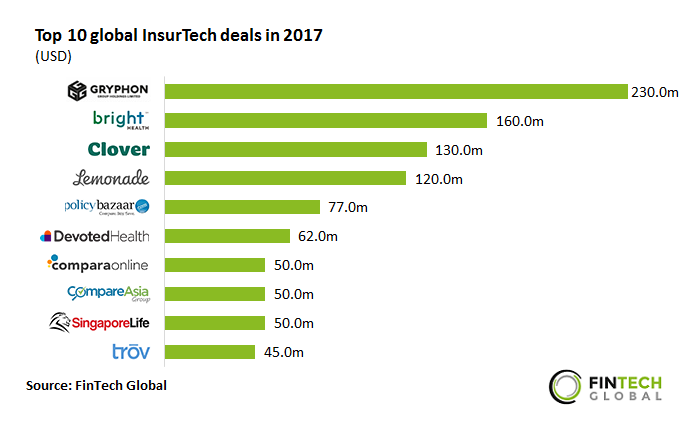

The top ten InsurTech deals in 2017 raised $974m, half of the year’s total funding

- The largest InsurTech deal in 2017 was the previously mentioned $230m investment in Gryphon Insurance. This was followed by a $160m investment in US-based Bright Health, a digital health insurance provider. Its Series B round was led by Greenspring Associates in Q2 2017.

- Six of the top ten deals were closed by companies based in the US. The remaining four investments were raised by companies in the UK, India, Singapore and Hong Kong.

- Three companies with funding rounds in the top ten provide comparison websites; PolicyBazaar, ComparaOnline and CompareAsiaGroup.