The total amount invested in Infrastructure & Enterprise Software companies globally in Q2 2017 was over double the amount invested in the previous quarter and up 155.8% YoY

- The total amount invested in FinTech companies in Q2 2017 rocketed to $1.69bn which is more than double the investment in the previous quarter. This was mainly due to a jump in the number of investments valued over $100m which increased from 1 to 7 between Q1 2017 and Q2 2017.

- While the huge jump in investment was a result of several large deals in Q2 2017 the total investment in deals valued under $100m has also seen an increase of 33.9% YoY.

- The number of deals to Infrastructure & Enterprise Software companies has consistently risen since the low of 48 in Q4 2016 but remains below the high reached in Q3 2016, when 73 deals were finalised.

2017 has already seen 12.5% more Investment than the whole of 2016

- 2017 is on track for a record year, outpacing 2015. The first half of the year saw Infrastructure & Enterprise software companies receive 77% of 2015 $2.27bn record investment total.

- The total investment in deals valued under $100m grew at a CAGR of 4% between 2014 and 2016 and looks set to increase again in 2017. So far 2017 has seen 63% of last year funding to deals valued under $100m.

- The number of deals remained steady between 2015 and 2016 despite the fall in total funding. The first half of this year has seen lower deal numbers with only 48.5% of the total number of deals closed in 2016.

In H1 2017 Infrastructure & Enterprise Software companies based in North America received more than three times the total funding to European companies

- North America consistently sees more than $1bn worth of investment to companies developing Infrastructure & Enterprise software. In 2015 this figure rose to almost $3bn, partly due to a $0.5bn deal to HR/ Payroll platform Zenefits in May 2015, however after falling by 58.8% in 2016, investment to the region looks set to recover by the end of this year.

- The total investment in Infrastructure & Enterprise Software companies based in Europe grew at a CAGR of 131.4% between 2015 and 2016. It has also grown again in the first half of this year, H1 2017 has already seen $100m more investment than the whole of 2016.

- Investment in Asian companies specialising in Infrastructure & Enterprise Software has had a very slow first half of the year with the region only seeing $33m of worth of funding, only 5.9% of the total it received in 2016.

The Top 10 Deals in H1 2017 raised a total of $1.5bn

- Nine of the top ten deals in H1 2017 were to companies based in the United States, with half of them to companies based specifically in the San Francisco Bay Area. The only company in the top ten based outside of the US is Avaloq, a Banking Infrastructure provider, based in Switzerland. The company received $353m of private equity funding in Q1 2017 from Warbung Pincus in the largest deal to the sector in the first half of this year.

- AvidXchange which develops software for accounts payable automation received second largest deal in H1 2017 and the largest deal within the sector in Q2 2017. Based in Charlotte, North Carolina the firm received a $300m private equity investment from Temasek Holdings, MasterCard and CDPQ.

- The remaining eight of the top 10 deals went to companies specialising in Security Technology.

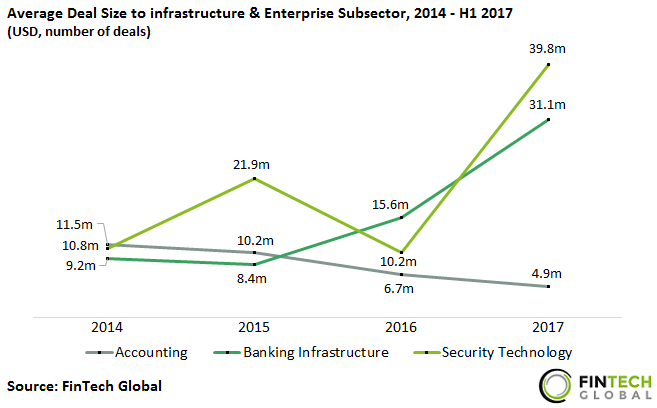

The average deal size to Infrastructure & Enterprise Software companies specialising in Security Technology rocketed in H1 2017

- Of the five Infrastructure & Enterprise Software sub-sectors Accounting, Banking Infrastructure and Security Technology received the highest number of deals between 2014 and H1 2017.

- The average deals size to companies specialising in Security Technology and Banking Infrastructure has increased over the years. The large deals to both these sectors outlined above caused the average deal size to hit records in H1 2017. In contrast, the average deal size to Accounting Software companies has fallen by an average of $1.96m per year.

- In H1 2017 the average deal size to companies specialising in Security Software was 28% higher than Banking Infrastructure and more than 8 times that of Accounting Software.