Germany’s FinTech sector has been steadily growing over the past six years, but investment levels have sky-rocketed in 2019. Is this the foreshadowing of the power shift from the UK to Germany post Brexit?

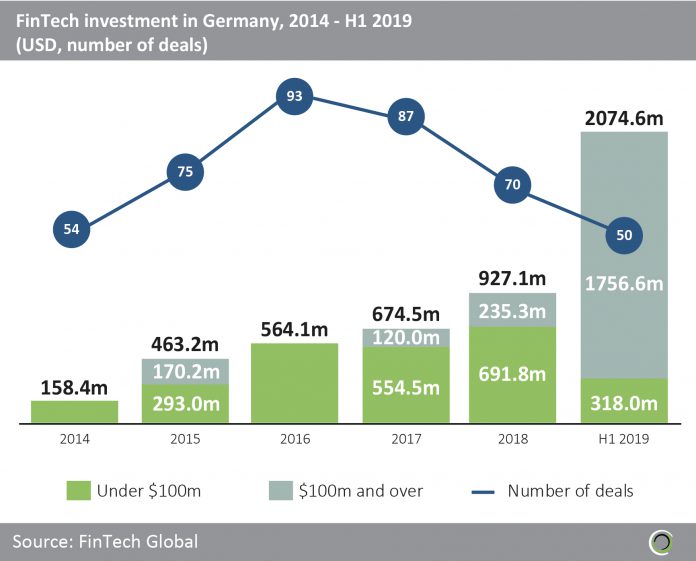

The FinTech sector of Germany has been second to the UK for many years, and while there is still a big difference margin, things could be shifting. FinTech Global data shows us the total amount of capital to be invested into the German FinTech space last year reached $927.1m, a steady rise from 2017, where $674.6m was raised. However, funding seems to have shot up, with the first six months of 2019 already seeing $2bn deployed to companies in the country.

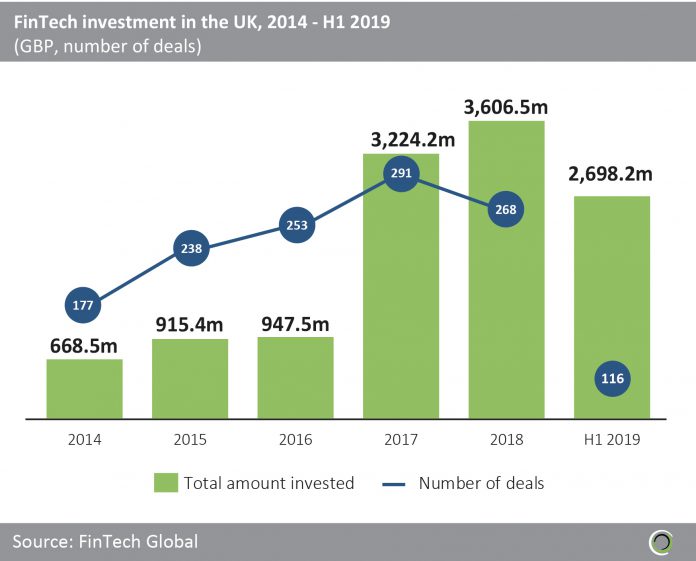

The UK and German FinTech markets were fairly close between the years of 2014 and 2016. However, the difference between the markets grew exponentially in 2017, when the UK witnessed $3.2bn invested into 291 FinTech companies and Germany only saw $674.5m deployed across 87 deals. The difference maintained its course in 2018; however, the first half of 2019 shows changes might be coming. In the first six months of 2019, $2.6bn has been invested into 116 UK FinTechs and $2bn has been funded to 50 FinTech transactions. The question is, will this rise in German FinTech continue and see the country become the new European home for the tech companies?

The UK and German FinTech markets were fairly close between the years of 2014 and 2016. However, the difference between the markets grew exponentially in 2017, when the UK witnessed $3.2bn invested into 291 FinTech companies and Germany only saw $674.5m deployed across 87 deals. The difference maintained its course in 2018; however, the first half of 2019 shows changes might be coming. In the first six months of 2019, $2.6bn has been invested into 116 UK FinTechs and $2bn has been funded to 50 FinTech transactions. The question is, will this rise in German FinTech continue and see the country become the new European home for the tech companies?

Temenos regional director for Central and Eastern Europe Noah Kraehenmann said, “In the first half of the year alone, at least 16 startups were merged or acquired. This is a trend that we are observing not only in the FinTech environment, but also in traditional banking. This trend is expected to continue over the next few years. It will also be interesting when global tech companies (GAFAs) seriously enter the market of FinTech companies, and thus banks and this could lead to a large shift in the sector.”

The German sector may have caught up in the amount of funding, but there is still a big disparity in the number of startups being invested into. The country’s great start to the year has been largely down to five companies which raised more than $100m in funding rounds – the largest of which was payment processor Wirecard’s $1.1bn post-IPO equity round. This suggests that the country has established some very strong FinTechs, but the other end of the market is still small compared to the UK.

Brexit has become an incredibly loathed word across Europe. Since the day of the vote, it has seemed to have worked into headlines everyday. Discussing how it will impact the financial market, what it will mean for farmers, who gets custody of the fish, and much more. Since the UK chose to leave the EU, various suitors stepped forward to become the new hub of FinTech. While the past few years have shown the market is staying strong in the UK, it appears there could be a shifting dynamic.

Regulations can be the good and evil of the financial market. While they help to improve stability and safety in the market, there are arguments it can stunt innovation. When the UK leaves the EU, its regulators will have a lot more responsibilities and there is likely to be various of changes to regulations businesses will need to get themselves around – leaving an opening for a stable regulatory market a little more appetising for a startup.

Kraehenmann added, “Naturally, changes to regulation for businesses based in the UK will impact the fintech sector. However, Germany has established a stable fintech eco-system in recent years, which continues to demonstrate growing maturity. It has become a hub for fintech innovation in its own right. Temenos currently works with German FinTechs such as Raisin and Kobil, through Temenos MarketPlace, Temenos’ digital app store for banks to connect with currently over 100 FinTechs. We see the German FinTech sector continuing to grow.”

Both the German and UK regulators have been taking an active role in supporting the FinTech space. The UK’s FCA has had a hands-on approach, ensuring there is a lot of support around regulations, and a regulatory sandbox to help companies test out their new services. The regulator was also one of the key members to support the launch of the Global Financial Innovation Network (GFIN). The body was formed by 12 international regulators with the goal of improving interactions between companies and regulators around the world and fostering innovation.

Likewise, Germany’s regulators have been making numerous efforts to support the development. In 2017, the country’s Federal Ministry of Finance launched a FinTech Council which is made up of 29 members to support innovation in the sector. The “FinTechRat” discuss relevant topics in the industry such as AI, cloud, and blockchain technology, and how to foster adoption.

Additionally, the Federal Financial Supervisory Authority (BaFin) has also looked to support FinTechs. It has established a specific team dedicated to FinTech and innovation and has hired various experts from the field to improve its oversight of the space. However, unlike the UK, the country has yet to establish a regulatory sandbox or a comprehensive regulatory approach.

Raisin UK CEO Kevin Mountford said, “While the UK still leads the charge for FinTech development, Germany (and in particular Berlin) is a fast-clipping at our heels.” Raisin is a European deposit marketplace which is headquartered in Germany but has offices in the UK. The company has brokered more than €14.5bn in savings for over 190,000 customers, since it was founded in 2012. The company is in the middle of both markets, and is showing the strength of German founded FinTechs, having closed a $114m Series D this year to support further internationalisation.

He added, “In addition, the EU’s move to foster growth by removing administrative friction in cross-border collaboration is another contributing factor to the growth of the sector in Europe. The European Union’s Payment Service Directive 2 (PSD2), has opened up banking APIs so that third-party offerings and long-standing financial institutions (like established banks) can experiment without sacrificing security that is afforded by bigger, and older, institutions like our partnerships with Legal & General in the UK. Newcomers do not need to compete but can rather pick up where incumbents have left off while continuing to transform and innovate the art of what’s possible.”

The outlook of the UK post-Brexit is still uncertain. With parliament set to suspended in a couple of weeks and Boris Johnson’s ambition for the UK to leave on October 31 no matter what, the next couple of months could be quite hectic and turbulent across Europe.

Copyright © 2019 FinTech Global