Investment in Singapore reached $1.6bn, 16.5% greater than investment in China in H1 2019

- Singapore, China, Hong Kong and India are Asia’s leading financial hubs which are all well positioned to become global leaders in the FinTech space due to their strong foundations in traditional financial services.

- In 2014, the majority of FinTech deals in Asia were raised by Chinese companies with 35.8% of all deals originating in the country. However, since 2015 the leading country in terms of deal share has been India with an average deal share of 31.9% over the period.

- In terms of investment, China has dominated the Asian FinTech space since 2015, however for the first time in H1 2019, Singapore has overtaken China with $1.6bn invested compared to $1.4bn in China. Further to this, Singapore’s deal share has increased to 22.0% in H1 2019, equalling China’s share.

- Singapore benefits from its easy access to regional markets which, coupled with tax benefits and government help make Singapore a more attractive choice for investors than rival hubs in Asia.

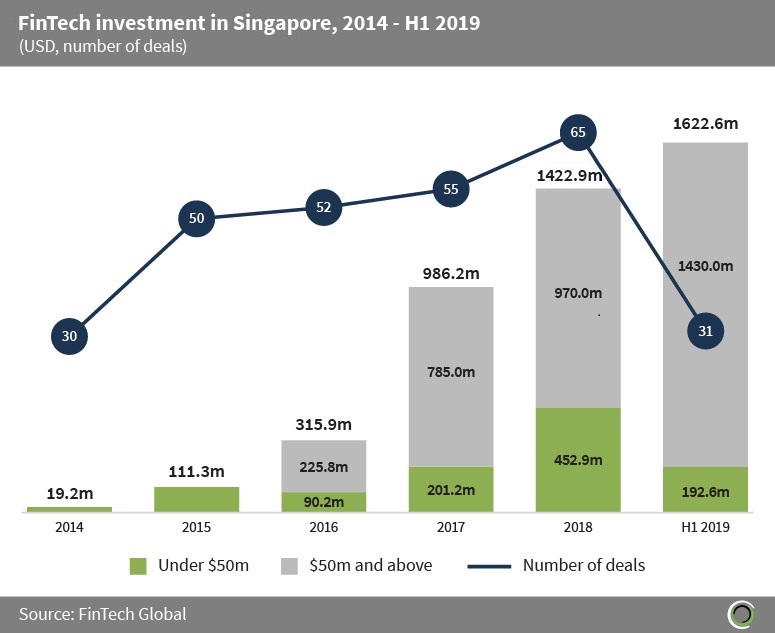

FinTech funding in Singapore has already surpassed 2018’s total in just the first six months of this year

- Over $4.4bn has been raised in Singapore across 283 transactions since 2014, increasing more than 84-fold over the period.

- Investment increased at a CAGR of 193.4% between 2014 and 2018, and this growth has continued into 2019 hitting a record total in the first six months of the year, accounting for 114% of last year’s total.

- The record investment in H1 2019 has been driven by Sea Limited’s $1.4bn post-IPO-equity round, accounting for 30.1% of total funding since 2014 alone. Upon exclusion of this record deal, H1 2019 has only raised 19.2% of 2018’s funding, setting investment to drop this year.

- 31 deals were completed in the first half of the year. If deal activity continues at the same pace for the second half of the year, deal activity should nearly match last year’s total and could exceed it.

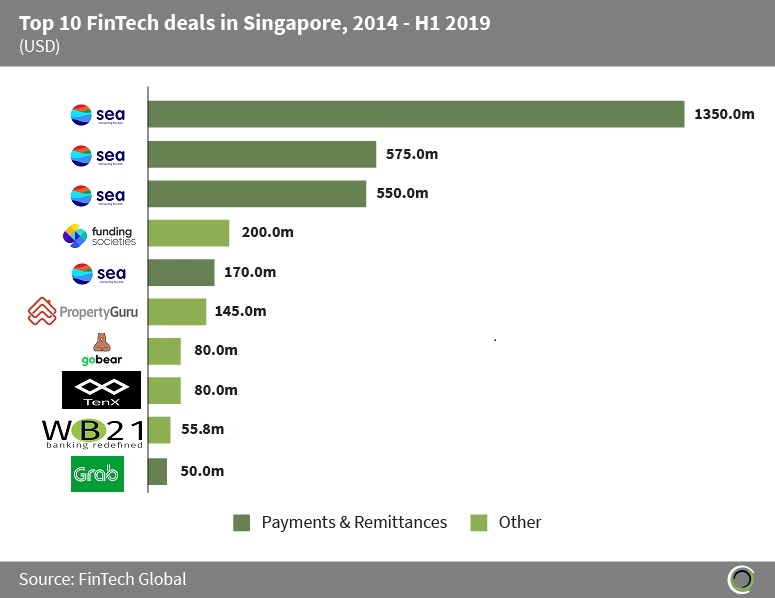

Over $3.3bn was raised across Singapore’s top 10 FinTech deals since 2014

- The top 10 transactions in Singapore have collectively raised over $3.2bn since 2014 which is equal to 74.4% of the total capital raised in the region during the period. This is a greater share when compared with the top 10 deals in China and India which accounted for 54.3% and 59.0% respectively.

- Capital allocation was diversely spread across sectors in the top 10 deals with four deals in the Payments & Remittances category, while Marketplace Lending, Real Estate, Cryptocurrencies, InsurTech, Blockchain and WealthTech companies accounting for one deal each.

- Sea Limited, a digital services provider whose products include e-commerce platform Shopee and e-wallet service AirPay, was responsible for four of the top 10 deals of the period, with three of these being the largest three transactions. The previously mentioned $1.4bn post-IPO-equity round was the largest deal of the period and the company plans to use the capital raised for business expansion and general corporate purposes, most likely focused on its e-commerce platform Shopee.

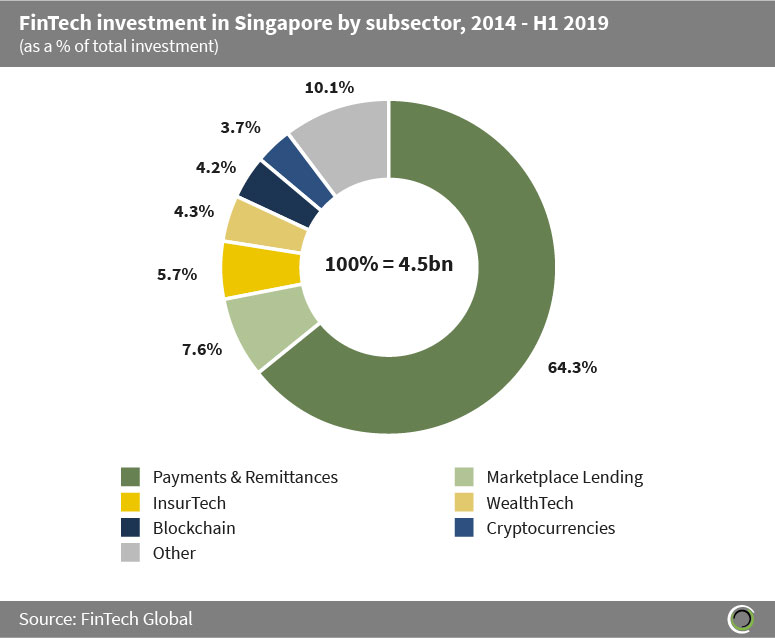

Over 60% of FinTech investment in Singapore has been raised by Payments & Remittances companies

- Payments & Remittances companies are responsible for 64.3% of Singapore’s FinTech investment between 2014 and H1 2019. Large investments in Payments & Remittances companies have been driven by the necessity to keep up with the rapidly changing payments landscape and the global trend of moving towards a cashless society which is especially popular in Asia and the Oceanic regions.

- Marketplace Lending companies are the next most popular choice for investment in the region with 7.6% of investment being raised by these companies. This comes after the financial crash of 2008 with new lenders looking to innovate the consumer loans market and capitalise on the distrust of mainstream banks.

- The other category includes companies in Real Estate, Data & Analytics, Institutional Investments & Trading, Infrastructure & Enterprise Software, RegTech and Funding Platforms subsectors, which collectively account for 10.1% of total capital raised in the period.

The data for this research was taken from the FinTech Global database. More in-depth data and analytics on investments and companies across all FinTech sectors and regions around the world are available to subscribers of FinTech Global. ©2019 FinTech Global