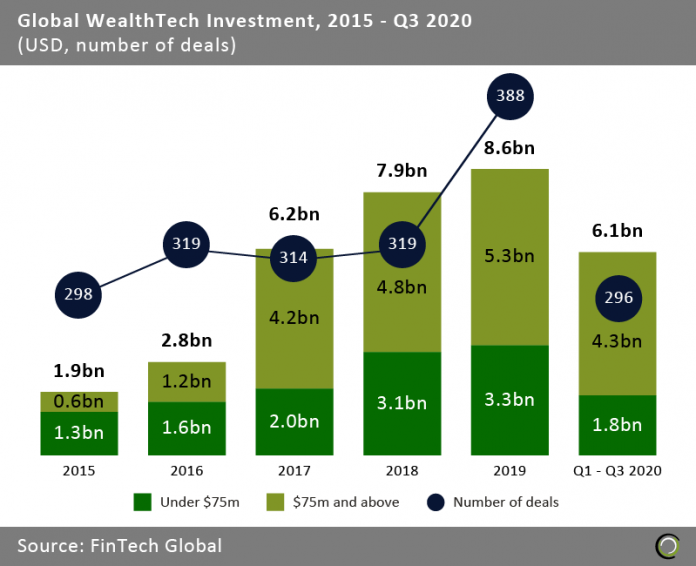

WealthTech funding in the first three quarters is 5.1% lower compared to the same period last year.

- WealthTech deal activity remained resilient in the first three quarters of 2020 and is higher compared to the same period last year. The period between Q1 and Q3 2020 recorded 6.5% more deals than observed in the same period in 2019. However, the total investment amount in WealthTech dropped by 5.1% when comparing the same periods with $6.4bn invested within the first nine months of 2019. This can be attributed to a trend of investment in smaller early-stage companies addressing new challenged in the industry post Covid-19.

- Funding for deals above $75m has steadily increased from 2015-2019 at a CAGR of 54.6% and even grew this year so far with $4.3bn invested, 5% higher at this stage in 2019. While investors are backing smaller companies they still support established WealthTechs which had a challenging year with millennial customers being negatively affected by the economic impact of the pandemic.

- In contrast, the total of $1.8bn coming from deals below $75m represents 30% of the total funding in the first three quarters of 2020 which is below the historical average of 47%. This signifies a decrease in average amount invested in deals under $75m in 2020, pointing towards a move to smaller deal volumes as investors are keener to back solutions addressing new pandemic challenges at the early stage level.

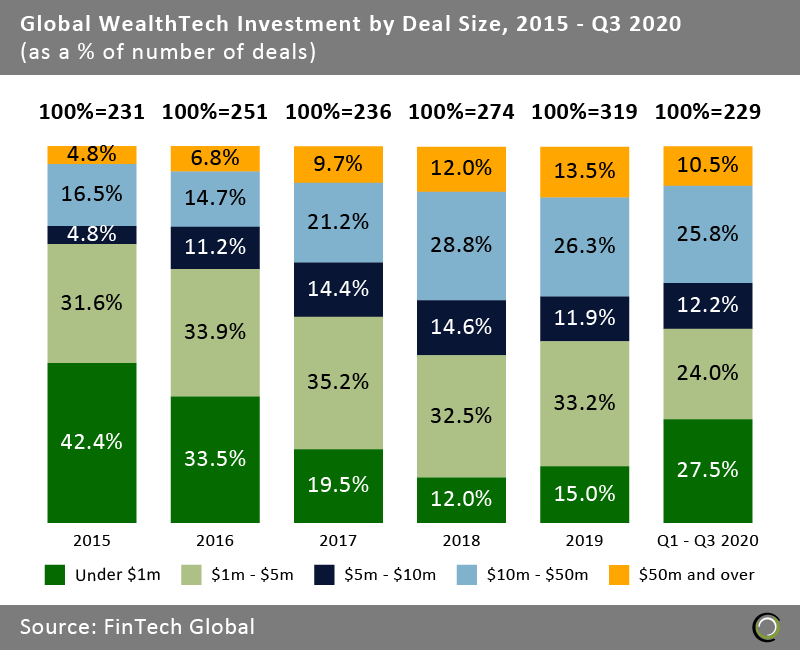

Deals under $1m on the rise, as investors favour early-stage investment during COVID-19

- This year saw an increase in the share of deals below $1m from 15% to 27.5% while the proportion of deals in the $1m to 5m range shrank by 9.2 percentage points (pp). This further supports the fact that WealthTech backers showed renewed interest in early stage smaller deals amid shifting market outlook post Covid-19.

- While the share of deals over $10m in 2020 declined by 3.5pp compared to the previous year, large deals still made up over a third of WealthTech investments. Due to loss of income established WealthTechs such as Monzo, which raised a £60m down round in June, needed financing to bridge the unexpected losses this year – hence still the strong presence of large deals, but not necessarily for growth purposes.

- The pandemic has accelerated WealthTech innovation as customers are unable to use in-person equivalents and has pushed for the move of the entire industry to digital. Remote working and overall worry over financial planning, on a corporate and personal level, will push for new solutions. This move towards innovation, rapid digitisation of banking, wealth management and advisory explains the strong deal levels and interest from investors.

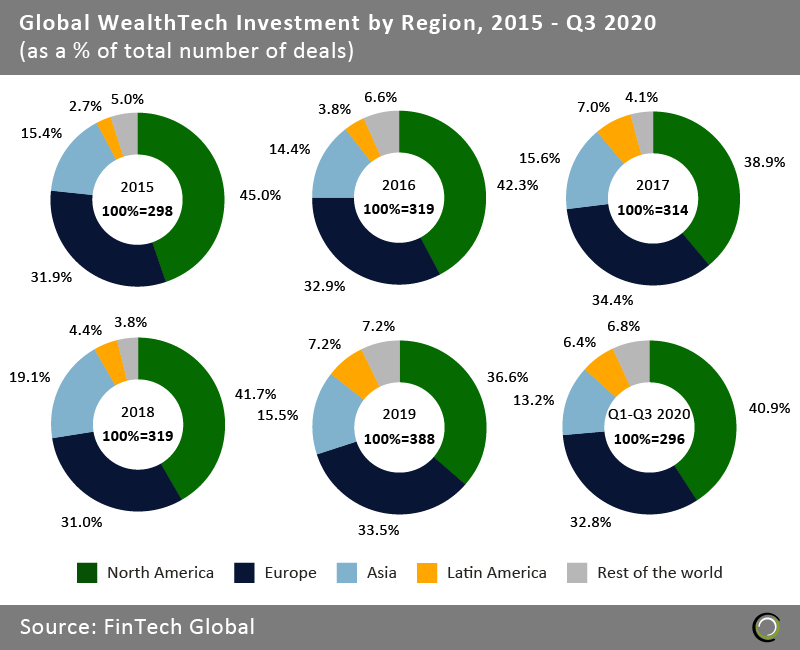

North America dominates WealthTech Investment as a location of innovation in 2020

- North America saw an increase in its share of WealthTech deals from 37% in 2019 to 41% so far this year. Historically, the North American market has been the breeding ground for WealthTech innovation. It is hence expected that it will benefit from an investment approach that favors early-stage investment. This growth can also be attributed in the move to remote working and recent deals in roboadvisors development. In a recent example of such early-stage investment in the region, The Wealth Factory raised $1m towards their mission of manufacturing economic independence for 1 million entrepreneurs.

- Asia is experiencing an all-time low in deal share in 2020, with companies in the region taking just 13% of total deal activity, a decrease from last year’s 16%, and 2018’s 19%. The decrease in 2020 is attributed to the fact that Asian markets were hit first by lockdowns and economic turmoil during the pandemic and the shift to established markets to support new innovation in the space.

- Latin America and Rest of the World have seen an increase in their deal shares over the past two years, from 4.4% and 3.8% in 2018 to 6.4% and 6.8% in the first nine months of 2020. This is a result of belated WealthTech development in these areas, which are finally claiming their market share. With largely unbanked populations and high adoption of mobile devices, these markets are primed for disruption. Growth is likely to be further accelerated because people are likely to shift their behaviour and increase their usage of digital financial services amid social distancing.

The data for this research was taken from the FinTech Global database. More in-depth data and analytics on investments and companies across all FinTech sectors and regions around the world are available to subscribers of FinTech Global. ©2020 FinTech Global