Customer background checks have again become a hotly debated topic in the cryptocurrency world.

Their detractors refer to them as surveillance exchanges. As the cryptocurrency industry is maturing, many exchanges have introduced processes to verify who their customers are in order to live up to know you customer (KYC) and anti-money laundering (AML) obligations. However, far from everyone trading with digital money is happy about the processes that they view as attacks on their privacy, as intrusions by Big Brother. Hence the unflattering soubriquet.

Part of the reason for the hostility originates in bitcoin and other cryptocurrencies’ long history of offering an anonymous alternative to centralised currencies. “[They] built their popularity on the premises of anonymity, trust and transparency,” Tom Albright, COO of Bittrex Global, the crypto exchange, tells FinTech Global. “These systems are designed to function without a need to trust or verify the identity of any particular counterparty due to encrypted wallets, public and private keys and the use of consensus mechanisms to verify transactions on a public ledger. As a result, these products were initially adopted by users seeking anonymity as a key feature.”

As a consequence, many crypto exchanges do not run tests to verify the identity of their customers or where they have sourced the capital. “Unfortunately, this initial belief in anonymity damaged the perception of blockchain technology and limited its mainstream adoption,” says Albright.

Indeed, cryptocurrencies have a gained a reputation for being used by criminals. This reputation is not entirely unwarranted. Over the years, bitcoin and digital money have been used on the darknet market Silk Road and as the payment method of choice for the laptop-wielding larcenists behind ransomware attacks. In Latin America, a cyber criminal industry has grown thanks to cryptocurrencies being used to launder money, according to a report by IntSights, the threat intelligence company, and CipherTrace, the leader in cryptocurrency intelligence.

And in 2019, an official of the United Nations argued that cryptocurrencies are making it more difficult to prosecute criminals guilty of cyber crime, terror financing, money laundering and abuse of children.

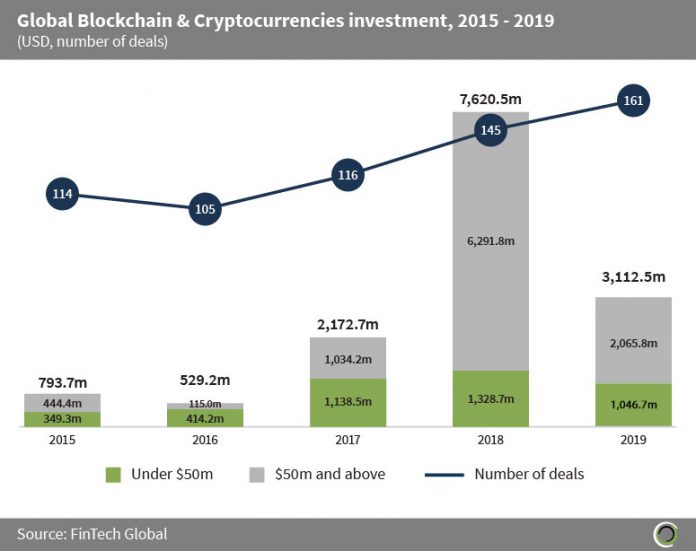

That does not mean that all cryptocurrencies and the people using them are criminal by nature. Neither does it mean that the exchanges where people can trade bitcoin, ethereum and ripple have anything nefarious about them. It would be ridiculous to argue that the blockchain and cryptocurrency companies that collectively raised over $14.2bn in global investment across 641 transactions between 2015 and 2019 would be linked to crime.

Yet, it does highlight a reason why exchanges like Bittrex Global have opted to introduce strict KYC and AML policies. “[These] policies are necessary for cryptocurrencies and blockchain technology to become widely adopted and to become key parts of the global financial system,” says Albright. He adds that Bittrex Global also continuously work to implement new technologies and best practices as they become available in order to improve these policies.

Another reason why many exchanges introduce KYC failing to do so would mean they’d fall foul of the law. More and more countries are requiring the people dealing with cryptocurrencies to have strict KYC and AML policies.

For instance, in the US, the Financial Crimes Enforcement Network’s (FinCEN) so-called ‘travel rule’ requires cryptocurrency exchanges to verify who their customer are, what the original parties and beneficiaries of transfers $3,000 or higher, and transmit that information to counterparties if they exist. In other words, they need to be KYC compliant.

These checks could also protect businesses, as Anthony Quinn, the founder of RegTech firm Arctic Intelligence, explains. He tells FinTech Global that failing to check who customers are and where their source of wealth from leaves exchanges open to be abused. “Without collecting, verifying and authenticating KYC information, as well as conducting due diligence checks like watchlist screening, enhanced due diligence for heightened risk individuals and entities, and re-screening of KYC checks, cryptocurrency exchanges and other regulated businesses unnecessarily expose their businesses to being exploited by bad actors,” Quinn says.

The need for KYC and AML have become even more pressing following hack attacks such as the one suffered by Binance in May 2019 when 7,074 bitcoins were stolen. On the day, they were worth roughly $40m, according to CoinTelegraph.

In the aftermath of the hack, the CEO of Binance Changpeng Zhao announced that the company was ramping up its security procedures. “We are improving our risk management, user behaviour analysis and KYC procedures,” he said. Although, Binance reportedly suffered another hack a few months later that supposedly compromised customers’ private data, which had been acquired during KYC checks. Not a great look.

Nevertheless, far from all customers have been happy with cryptocurrency exchanges pushing for enhanced KYC and AML. Several users have complained about it on Twitter and Reddit. When BitMEX advertised for an AML director in March 2020, several detractors were quick to predict it would mean the end of the exchange.

Albright says that if customers are unhappy with complying with Bittrex Global’s KYC and AML procedures should “look elsewhere.”

However, the sentiment is not shared by everyone. When Digitex suffered a breach earlier this year that compromised its customers’ data, the CEO Adam Todd responded by cutting off all KYC checks for the exchange. Noting that this would mean trading in the US would become illegal, Digitex banned US-based users from using the service by restricting American IP addresses and making people check a tick box to say that they are not from the country.

When explaining his decision, he argued that the notion that people would use crypto exchanges to launder money was “ridiculous.”

“People are not laundering Ethereum into DGTX to fund international terrorism,” Todd argued. “[I] just sound stupid even saying that statement. It’s fucking ridiculous to even say it. So I am not going to waste your time talking about that side of the argument. It is obvious bullshit. It’s a crook of shit and I am calling it out for what it is.”

In other words, it clear that the issue of KYC and AML for cryptocurrencies is won’t be resolved yet for some time.

Copyright © 2020 FinTech Global