FinTech startup Jiko has acquired Mid Central National Bank in a deal that is the first of its kind.

The startup has become the first in its sector to acquire a US-regulated bank, according to CNBC.

Founded in 2016, Jiko has moved pretty much under the radar until now, only raising a $7.7m Series A round in October 2017.

But now it has shaken up the sector by buying the 63-year old Minnesota bank, according to sources familiar with the transaction.

The participants of the deal have secured approval from the Office of the Comptroller of the Currency as well as the Federal Reserve Bank of San Francisco.

The deal gives the challenger bank huge access to the highly regulated US market.

As FinTech Global has reported in the past, getting access to the US banking market is far from easy.

Most digital banks such as domestic ones like Chime or European rivals like Revolut and Monzo opt to team up with FDIC-backed institutions to be able to offer regular banking services.

This is usually seen as a faster way than having to apply to become a chartered bank, a process that can take years.

That being said, Varo Money successfully became the first neobank to earn a banking charter in August.

Now it seems that there is a third way available, to purchase an existing bank like Jiko did.

“The move by Jiko represents an important milestone in the maturity and evolution of FinTech companies seeking to expand the reach of their products and services,” said Brian Brooks, acting Comptroller of the Currency, in a statement seen by CNBC. “It demonstrates the value and attractiveness of banks and in particular the federal banking system.”

The publication reported that one of the main reasons why regulators are okay with the deal is because Jiko’s business model is not holding deposits.

While customers’ cash are initially put into an FDIC-insured account, they are quickly put into Treasury Bill that are in turn liquidated when a person uses their debit cards or withdraws money.

To Stephane Lintner (pictured), CEO and co-founder of Jiko, the deal highlights people’s changing relationship with their money.

“The past decade of FinTech and online banking innovations has exposed new customers to our industry and demonstrated that innovation in the financial sector is needed,” he said.

“People’s relationship to money must be fundamentally improved for everyone. One of Jiko’s primary goals is to give people what they deserve: more organic and direct returns, without intermediaries and unnecessary friction.”

The news about Jiko’s new deal comes as the global neobank market is predicted to be in for some remarkable growth in the next few years.

In 2019, the sector was expected to be worth $20.4bn. That figure is estimated to grow to reach $471bn by 2027, according to a recent ResearchAndMarkets.com report.

The growth is said to be driven by increasing governmental and regulatory support towards the sector as well as higher interest rates offered to customers over that given by traditional banks.

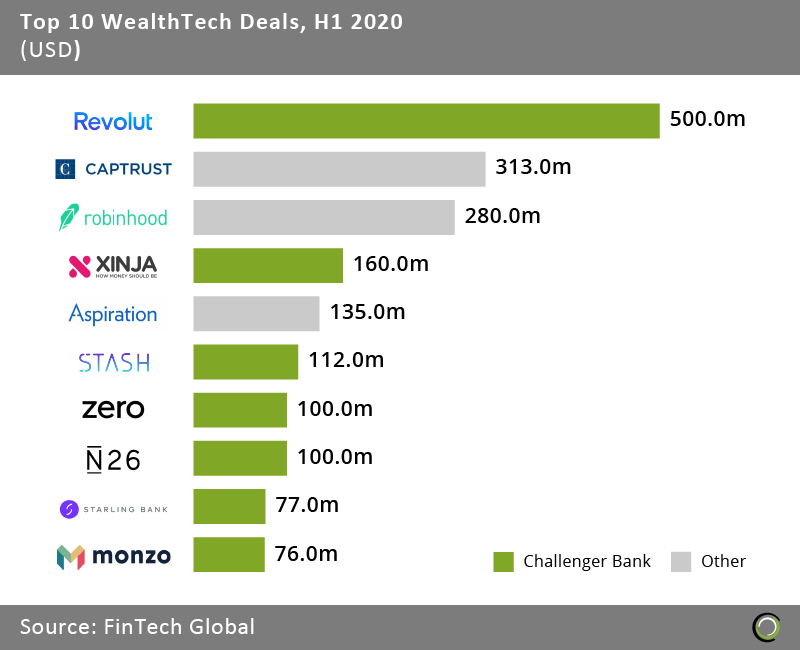

Challenger banks account for a big part of the investment going in the WealthTech sector. In fact, seven of the biggest deals in the sector in the first half of 2020 were in the digital banking sector, according to FinTech Global’s research. Those deals were Revolut, Xinja, Stash, Zero, N26, Starling Bank and Monzo.

However, all estimates about the sector should be taken with a pinch of salt as long as the coronavirus pandemic rages on across the globe.

However, all estimates about the sector should be taken with a pinch of salt as long as the coronavirus pandemic rages on across the globe.

In the UK, three of the biggest challenger banks – Revolut, Monzo and Starling Bank – have all recently reported that they had doubled their losses over the past year.

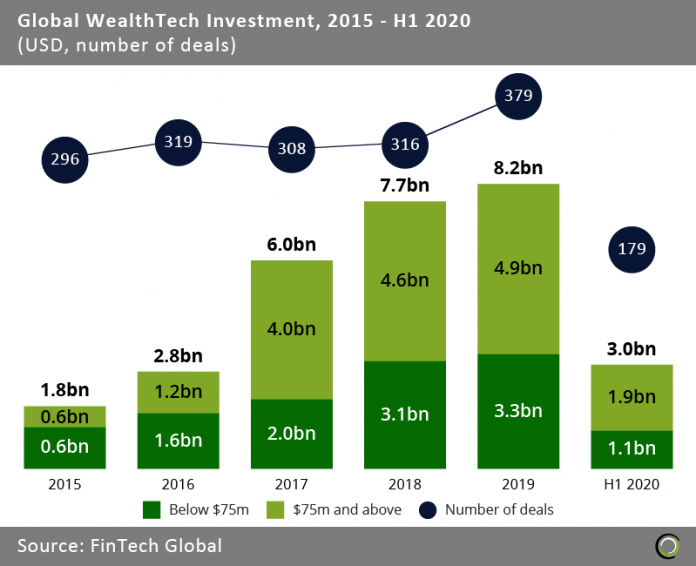

If we look at the WealthTech sector as a whole, it seems as if it could be en route to endure one of the worst years of investment since 2017 when the industry raised $6bn.

That would mean the end of a long winning streak for the sector. Back in 2015, the global WealthTech sector attracted $1.8bn across 296 rounds. Over the next four years the number of deals and the amount injected into the industry grew expectationally until the record year of 2019 when investors invested $8.2bn across 379 deals into WealthTech companies.

Then 2020 happened. Covid-19 has destroyed many people’s access to the disposable income. This has been especially true for millennial customers, which WealthTech businesses rely on. In the first half of 2020, the sector only saw the completion of 179 rounds and a total of $3bn being injected into the sector.

Copyright © 2020 FinTech Global

Copyright © 2020 FinTech Global