UK challenger bank Tandem is getting rid of its credit card line since it proved too costly and will now pivot towards homeowner financing after potentially having suffered a down round.

Sifted broke the story yesterday, revealing that the neobank would now double down on expanding its savings accounts offerings and use the money accrued to fund mortgages and home improvement loans.

Ricky Knox, CEO of Tandem, told Sifted that the bank has no desire to follow in the footsteps of rivals like Revolut, Starling Bank and Monzo who have all reported massive losses in their annual financial reports.

The Tandem CEO also claimed that its losses would not be as severe as the one recorded by its peers when the neobank releases its annual results in the next few weeks.

Sifted also noted that the £60m fundraise Tandem made in August, helping it acquire green lender Allium, saw new investor Pollen Street Capital inject £14m into the business. The publication confirmed that the private equity firm’s investment had earned it a 15% stake in Tandem.

This suggests that the company’s valuation had dropped by 40% to roughly £90m, having previously laid around £150m.

If true, Tandem is not alone in having suffered a down round this year. Monzo raised a £60m round in June that saw its valuation drop by 40% from $2bn to $1.24bn.

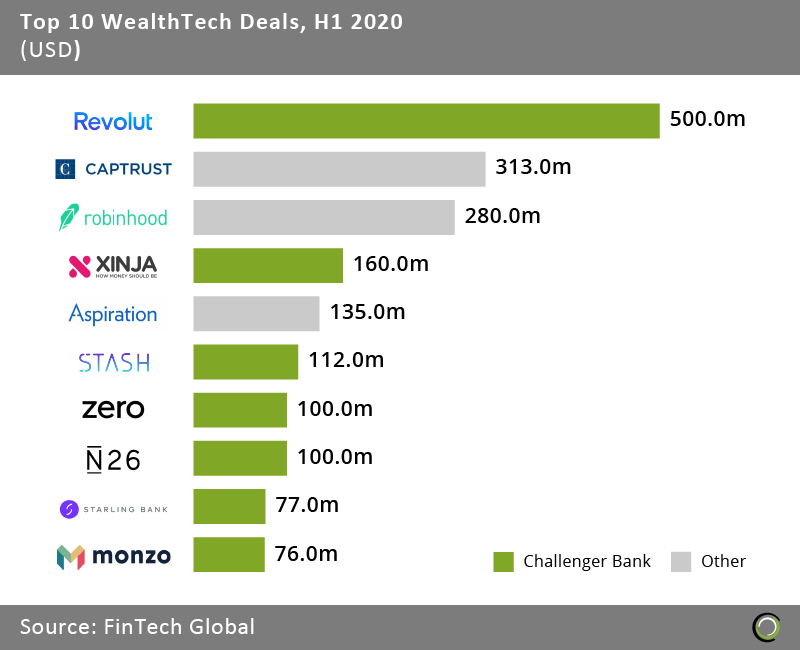

Challenger banks are a huge segment of the WealthTech sector, with seven of the biggest deals in the sector in the first half of 2020 having been in the digital banking sector. Those deals were Revolut, Xinja, Stash, Zero, N26, Starling Bank and Monzo, according to FinTech Global’s research.

However, the massive losses reported by three of the biggest UK neobanks are not the only problems noted in the WealthTech sector.

However, the massive losses reported by three of the biggest UK neobanks are not the only problems noted in the WealthTech sector.

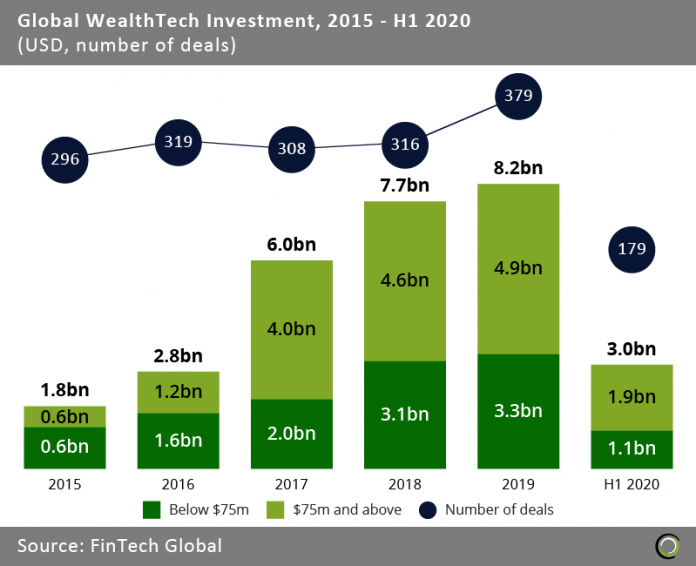

In fact, the sector could be heading towards its worst year since 2017 because of the ongoing pandemic. Covid-19 threatens to break the winning streak seen in the last five years by slashing the disposable income for people across the world, especially among the millennial segment that the businesses in the sector rely on.

Back in 2015, the global WealthTech sector attracted $1.8bn across 296 rounds. Over the next four years the number of deals and the amount injected into the industry grew expectationally until the record year of 2019 when investors invested $8.2bn across 379 deals into WealthTech companies.

Then 2020 happened. In the first half of 2020, the sector only saw the completion of 179 rounds and a total of $3bn being injected into the sector.

Copyright © 2020 FinTech Global

Copyright © 2020 FinTech Global