The Nordics in general and Sweden in particular are experiencing a FinTech boom. However, new regulations and investment worries could slow down the growth.

Sweden’s future is digital. Swedish entrepreneurship is about more than IKEA, H&M and Volvo. In the last three decades, the nation has remade itself into an innovative technology hotbed. Spotify, Skype and iZettle are all examples of successful digital ventures to come out of the country.

FinTech innovators are driving a lot of the success. Klarna’s $460m investment round last summer pushed the PayTech unicorn’s valuation past the $5.5bn mark, arguably making it Europe’s most valuable FinTech scaleup and cemented Sweden and the Nordics’ position as industry leaders.

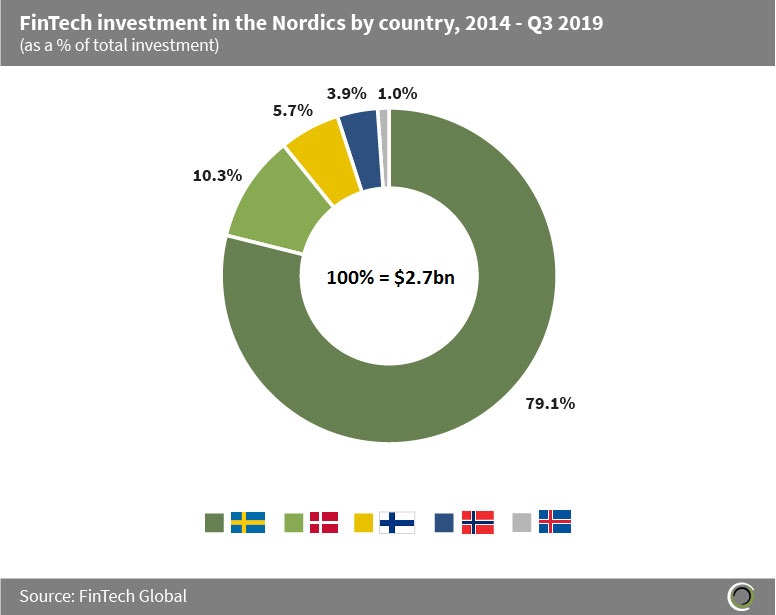

Not that anyone needed much convincing. After all, Swedish, Norwegian, Danish, Finnish and Icelandic FinTech companies have together raised over $2.7bn since 2014, according to FinTech Global’s data. Sweden has picked up over 79.1% of that investment, followed by Denmark, which attracted 10.3%. Finnish FinTech firms raised 5.7%, Norwegian ones 3.9% and Icelandic enterprises 1%.

Lana Brandorne, co-founder of Sthlm Fintech Week, is unsurprised by Sweden’s position as the Nordic FinTech flagbearer. “Sweden has historically had a lot of success stories that today are paving the way for Sweden to be seen as one of the most innovative countries in the world,” she tells FinTech Global.

The Swedish government’s early technology support is a key factor to this success. “The Swedish government pushed out a widely developed broadband network in the 1990s and early access to fast internet coupled with subsidised computer-lending programmes helped cultivate a society of early adopters,” Brandorne continues.

Moreover, education in Sweden has given the ecosystem a huge boost. The educational system in Sweden is free and ranks above average compared to other OECD countries. Additionally, the interdisciplinary focus of the education is aimed at encouraging innovation. Initiatives like these have led to 18% of Stockholm’s citizens now working with tech.

“It is a secure social system allowing people to take more risks,” argues Brandorne. “Substantial social benefits reduce the risks faced by entrepreneurs and costs for companies, thus encouraging startups.” Sweden’s developed IT infrastructure and high-quality education have given the country an early mover advantage over its neighbours.

The nation also has a bigger domestic market than the rest of the Nordics. Sweden has a population of over ten million people whereas Norway, Denmark and Finland all have just over five million citizens each. There are only about 362,900 people living in Iceland.

Additionally, Sweden has an extremely strong economy. Swedish lawmakers introduced massive economic reforms after the country suffered from a financial crisis in the early 1990s. These included putting a cap on public spending. The measures were backed across the political spectrum and have yielded impressive results, with the national debt having dropped from 69.5% of GDP in 1996 to 35.1% in 2019.

Today, the World Economic Forum has ranked Sweden as the seventh most competitive country in the world, the World Bank named it the tenth easiest country in the world to do business in and the three of the world’s leading credit rating companies – Fitch, Moody’s and Standard & Poor – have given the country an unusual AAA rating.

The bullish economy, the governmental support, the free high-quality education and Sweden’s far-reaching social policies have all contributed to creating a nurturing environment for tech entrepreneurs. “Stockholm has an innovative ecosystem of academia, corporates and startups together with a culture of diversity, gender equality as well as an outstanding welfare system, which attract talents from all over the world,” Anna Blyablina, co-founder of Sthlm Fintech Week, tells FinTech Global.

Brandorne adds, “The trust in the financial ecosystem and technology have allowed for new digital financial products to immerse and be adapted rather fast. This can be seen in the sheer number of FinTech companies registered in Sweden.” There are roughly 400 FinTech companies in the Swedish ecosystem.

Their impact is evident in the country’s adoption of cashless solutions. “Cash usage is declining in Sweden,” says Blyablina. Indeed, only 13% of Swedes used physical money for their last purchase and 60% thought that they might have used it sometime in the last month, according to Sveriges Riksbank’s 2018 payment pattern report. Comparatively, 28% of all payments in the UK, which is hailed as the FinTech leader of Europe, were made with cash that year, according to UK Finance. Researchers from the Swedish Royal Institute of Technology estimate that Swedish retail will basically be entirely cashless by 2023. It should be noted that similar trends can be seen in the other Nordic nations too.

Swedish innovators also benefit from a supportive ecosystem. “Only Stockholm alone has around eight FinTech-focused initiatives and every year the support for the startups increases within the FinTech ecosystem,” says Blyablina. “On the broader picture Nordics are home to several accelerators, incubators, hubs and labs. In recent years, several new players have been established and currently, one can find help at any stage of the company, be it an idea or a scaleup and anything in between.

“As the industry has a collaborative approach the FinTech initiatives follow this lead and Sthlm Fintech Week, among other Nordic Fintech hubs, has established the Nordic Alliance with the focus of sharing the knowledge and support FinTech startups in their journey. And while success stories defining this lead are plenty, what distinguishes Sweden amongst tech hubs globally is the celebration of a community which facilitates an ecosystem that breeds the spirit of sharing.”

Swedish banks have also, whilst initially being very protective of their own businesses, begun to partner up with the new FinTech companies. “Collaboration and partnership are something Nordics have been good at initiating,” says Blyablina. “Having a collaborative approach is a very common feature in the Swedish mentality. There are cases such as BankGirot, BankID, Swish and now there are Nordic joint projects, such as P27 and Nordic KYC.

“Then comes the symbiotic bank-FinTech relationship. Dynamic and customer-focused FinTechs are better able to adapt to the changing needs of the market, but they struggle to succeed on their own. On the other hand, traditional banks are facing increasing challenges due to their legacy IT systems and outdated cultures. The banks need FinTechs to innovate. The collaboration between banks and FinTechs is likely to increase efficiency in the ecosystem.”

New Swedish FinTech startups also benefit from not being the original movers on the scene. Many new FinTech entrepreneurs in Sweden either cut their teeth working at successful FinTech unicorns like Klarna, Bambora and iZettle or at the nation’s big banks. “That’s what we call second-generation unicorns,” says Blyablina. “And at the same time, it is also common for the successful actors to invest back in the ecosystem so that the circle is closed. We can see a lot of former employees of these unicorn companies creating their own ventures. Moreover, a lot of second and third-generation entrepreneurs, who have been through the rollercoasters are ‘paying it forward’ and are investing in and coaching some of the younger entrepreneurs.“ What comes around goes around, basically.

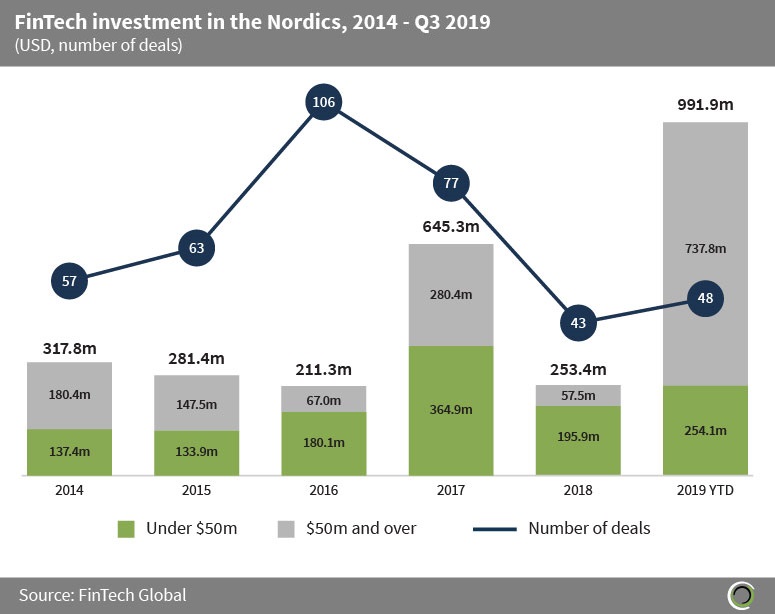

Swedish FinTech companies still face many challenges. One has to do with accessing money. Investment injected into the ecosystem tripled from $308.3m in 2014 to $991.9m in the first nine months of 2019, according to FinTech Global’s data. The average deal size grew from $5.6m to $20.7m during the period, indicating that the landscape is maturing.

“However, there is a big gap between highly valued companies attracting multi-million funding rounds and early-stage startups who are looking for seed and A round investments,” explains Brandorne. “Definitely, there is space in between that is currently underserved and international investors could potentially help companies to take their next step.”

FinTech startups in the region must also deal with growing pressure from regulators. “The increasing demands from the regulator are certainly adding a level of complexity and strains on FinTech companies globally, thus Nordics are not an exception to this,” says Brandorne. “Many struggle to adapt all the compliance requirements.”

The recent e-commerce rules proposed by the minister for financial markets, Per Bolund, provides an example of new regulatory hurdles to overcome. He suggested a ban against having buying things on credit as a pre-ticked option when buying things online. Bolund argued that this would prevent people going into debt by spending money that they did not have. “It will mostly affect the larger players like Klarna and Qliro who offer check-out solutions and have their own credit offers,” says Brandorne. “These are particularly popular with merchants since the aforementioned companies undertake the risk of customers not paying.” Unsurprisingly, Klarna has opposed the proposal.

Yet, Brandorne downplays this type of interventions. “In Sweden, it’s rare to see the government steer these kinds of details, but we have seen it in Germany,” she says. “The reason that this has appeared on the government radar has to do with the fact that the younger generations are overestimating their power to pay back and thus end up in endless credits.”

Nordic FinTech companies also struggle with the size of the market. “Additionally, for most consumer facing products, the home market is too small for most companies,” says Brandorne. “While this is a challenge, it is also an advantage since companies must consider going global since day one.“

While these challenges are undoubtedly huge, Brandorne is confident the Swedish FinTech scene will come out on the other side. “Stockholm is booming,” she concludes. “The FinTech playground is growing and new players are coming up all the time. We think, even more capital will be attracted into the region and the number of companies with a global presence that are #NordicMade will grow and gain recognition.”

Copyright © 2020 FinTech Global