Neobanks in the Nordics may have had a slow start, but things may soon be about to change.

Challenger banks in the Nordics are about to become a massive thing. A number of FinTech startups have launched across the Scandinavia over the past few years. While none of them have really gained the same traction as their cousins and rivals in the UK, Germany or the Netherlands, they are slowly starting to pick up speed.

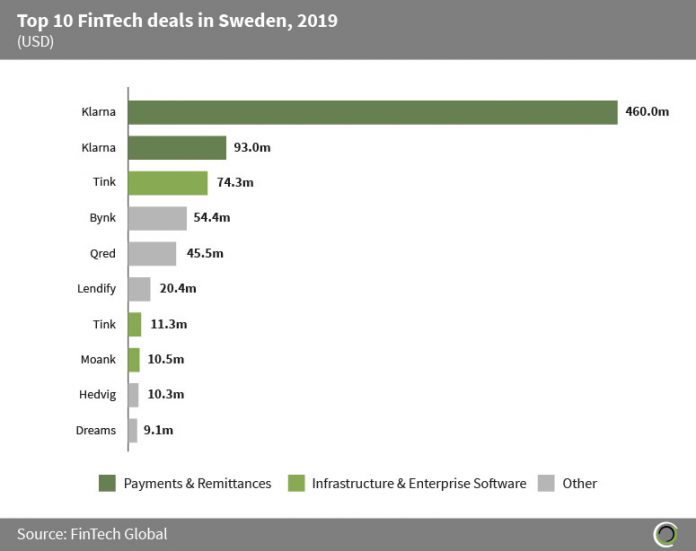

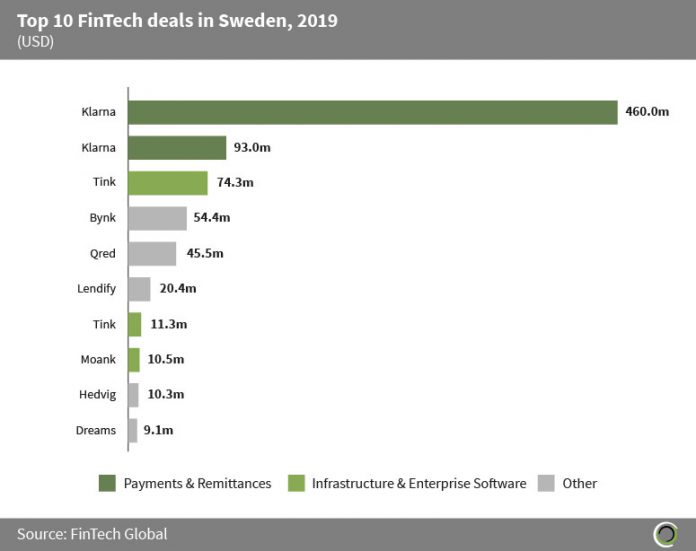

Danish digital bank Lunar raised €26m and secured a banking licence in August 2019 and its currently live in Denmark, Sweden and Norway. In Sweden, neobank Northmill was granted a banking licence in September and has since launched a new card and a savings account. Rocker, formerly known as Bynk, raised the fourth biggest FinTech investment round in Sweden in 2019. The round was worth $54.4m. Icelandic indó launched in 2018 to “shape the bank of the future.”

It’s no secret why these initiatives have launched. “All of us have been trying to fix an underlying problem,” said Oscar Hyléen, deputy CEO and head of communications at Rocker during a panel at Sthlm Fintech Week. “The fact is that there’s been an outcry for increasing competition for 30 years across Europe. And [the reason why it’s] happening right now [is because] traditional banks, as we know, have underperformed [towards] the customers and they have overcharged them. And so that is the reason why we exist.”

The launch of the new batch of digital banks comes as things are changing for Nordic banks. The incumbents in the region have long been considered strong and stable. The anti-graft group Transparency International used to rank Sweden and Denmark among the least corrupt countries in the world.

However, confidence in Nordic banks has taken a tumble because of a series of money laundering scandals. Chief among them is the Danske Bank scandal, which has been named one of the biggest European banking scandals ever. In 2018 it was revealed that about $223bn in suspicious transactions had been processed through the Danish lender’s systems. Several of the bank’s executives have been arrested, the CEO has left the company and more than 18,900 customers have abandoned the lender. Investigations into the Danske Bank’s wrongdoings are still ongoing.

It was not just Danske Bank that was affected by the scandal. Swedbank, which processed some of the transactions, also ousted both its chairman and CEO, and has seen its earnings plummet in the aftermath of the affair.

Nordea, the biggest bank in the Nordics, has also been investigated for suspicious transactions taken place through its bank.

Additionally, Danske Bank also improperly charged 87,000 of its customers for the Flexinvest Fri product.

These examples make it easy to see why people may have lost confidence in the Nordic incumbents.

For the new Nordic challenger banks, this crisis in confidence in traditional financial institutions could be a way for them to get a foothold of the market. After all, a wave of Australian neobanks leveraged the confidence crisis Down Under – initiated by the misconduct findings of the Australian Royal Commission into Misconduct in the Banking, Superannuation and Financial Services Industry – to launch their ventures in the country.

But to successfully take advantage of this opportunity, Nordic challenger banks must ensure the public trusts them. Understandably, the Sthlm Fintech Week panel was also asked point blank how they would create that trust.

“The last couple of months or years, it has been the AML, [anti-money laundering,] issue that has really picked up a lot of headlines in newspaper and the whole KYC, [know your customer,] issues as well,” answered Morten Sønderskov, COO at Lunar during the panel. “And then we have the whole data coming up with the GDPR. I think, speaking from our side, our approach to that has been our ability to start [with] a clean [slate].” Lunar has thus made an effort to create a backend system where the challenger bank is in full control of all data points and to ensure that it is “completely transparent” in what it does with the data.

Eli Keren, co-founder and CEO of P.F.C., a personal finance app, who also sat on the panel, added that his enterprise is trying to build trust by educating its customers on how to better manage their money in order to build trust. “If you have that two-way dialogue with your customers, you build up that trust,” Keren said. “It’s not going to happen [on] Day One, but it’s a long-term game for us. We always have to prove that we can do the job.”

However, launching a new bank, digital or otherwise, is a tough task to take on. Not only must entrepreneurs in the sector compete with both incumbents and other startups, but they also have to navigate a complicated web of regulations.

“We got our real banking license [in] August last year and [it] was [one] hell of a process just to get that,” said Sønderskov. “I think that I speak for all of us when I say that we may have been two steps ahead of the regulation.” He said that Lunar had gone through the experience feeling as if regulators did not really know what to do with them. “They did not actually have the regulation in place to deal with companies like us in the first place,” Sønderskov added.

He also said that the process had helped the regulator define the challenger bank segment. The Lunar COO also added that it had also negotiated with the Financial Services Authority how to regulate “cloud providing or using cloud service as a bank,” which Sønderskov said “was a completely new page in their book and that was two and a half years ago.”

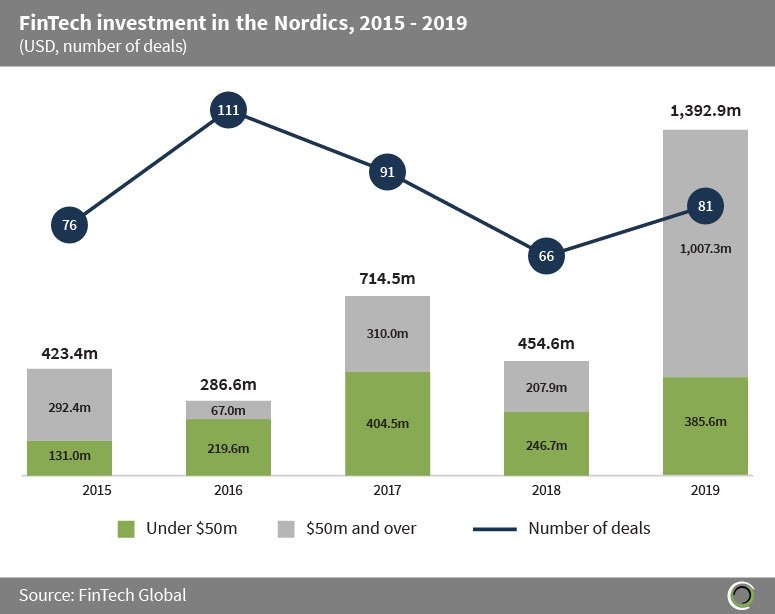

Challenger banks in the Nordics are not just competing with traditional lenders, but also with more established FinTech ventures. The Nordics in general and Sweden in particular have become a FinTech hotbed in the last decade. The region has attracted almost $3.3bn of investment since 2015, according to FinTech Global’s research. Swedish companies captured 78% of that money.

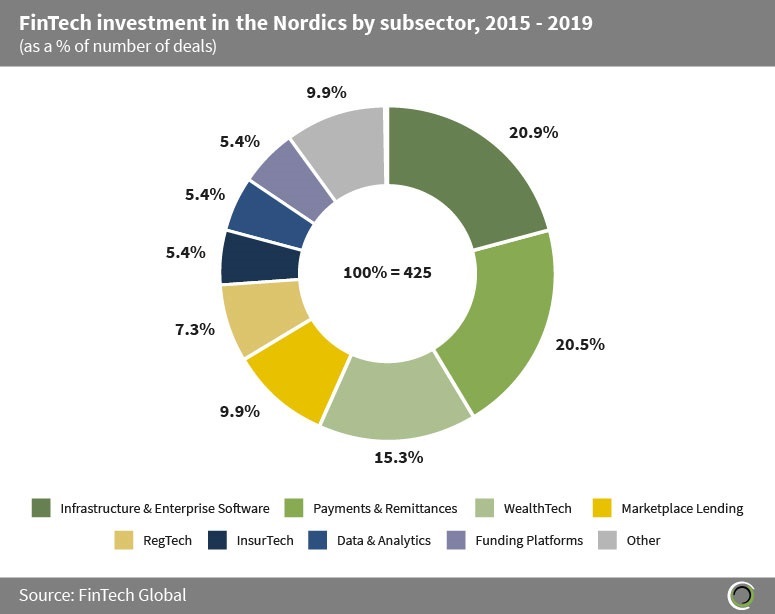

Of that capital, 20.9% were raised by infrastructure and enterprise software ventures, 20.5% by payments and remittances companies and 15.3% went to WealthTech companies, which is the subsector challenger banks are part of.

There is no shortage of FinTech success stories in the Nordics. Buy now, pay later unicorn Klarna arguably became Europe’s most valuable FinTech company in August 2019 when it achieved a $5.5bn valuation after its $460m equity round. Swedish banking portal Tink raised €90m in January 2020 to fund its European rollout. In 2018, PayPal acquired point-of-sale iZettle developer in a $2.2bn deal.

And that is where the new neobanks may face a challenge. “I don’t think we should underestimate the payment companies,” said Oscar Lidbeck, head of business development and the FinTech Innovation Hub at Svea Ekonomi, the Swedish financial services company, during the Sthlm Fintech Panel.

“Because they have a lot of users and they have [a good grasp of] the whole transaction from the beginning when you’re thinking about buying something to when you have things to purchase. And they have a lot of information around these transactions as well so that they can present it in a very nice way [that’s] more like entertainment than [administration].

“So I think that they’re well positioned to handle your daily economy and I think that, also, the young people they will [probably] go to Klarna to get their first mortgage or credit. That’s more likely to happen [than them going to a] neobank. I think we have a lot of competition [from them and] we need to learn from them [about] how to present things and how to manage our services.”

But what would a challenger bank need to be successful in the Nordics? “Speed is a major challenge,” said Hyléen. “I think this [is a] winner takes most race.” Pointing at the UK digital bank Revolut, which recently reportedly raised a $500m round, Hyléen noted that the bank had gained its seven million customers since the launch in 2015. “So speed is of the essence,” he continued.

Hyléen also noted that neobanks need to possess persistence. “You have to if you’re in this race [and] I think you have to be in for the long run,” he said. “It will take time to change consumers behaviours. We all know that, I think. You have to have consistency. You have to have money to be able to do that.”

The one thing none of the panellists seemed to worry about was their ability to monetise their product. “It’s not a question about [if] people are not willing to pay for the services,” said Sønderskov. “They do it today already. If you look across the Scandinavia, we see a very lucrative market in the financial services [market].”

He added that while many of the new players in the banking sector have entered the market with free products, challenger banks can also roll out other products like loans and mortgages services where they can make money. “If we succeed and when we succeed, we will launch a full product portfolio, reflecting all the financial products that you’re actually aiming for or looking for,” Sønderskov continued.

Keren agreed and added, “Most industries today are digitalised, except this space. I mean, nothing has happened or changed for consumers in the last, what, ten years. [It’s] the same apps from banks [now as when I started]. That’s our job. We’re trying to build great digital products and business models. You have classical banking products and then we’re innovating on top of that. [We’re] launching subscription models. [If there is] a bank that [has a] phenomenal [subscription service then I] haven’t seen it. So it’s obviously coming out from [the] digital space.”

The P.F.C. co-founder explained that challenger banks focus on the technology has enabled the startups to rapidly roll out improvements to their user experiences and new products. “We launched products within three months [and] that’s unheard of in a private industry,” he said. “So I think [that] sometimes you look at what we do a little bit too easy. It’s very complex on the front and on the backend. And I think that is the real innovation.”

Copyright © 2020 FinTech Global