The UK is home to one of the world’s most thriving FinTech and RegTech communities, but Brexit has raised concerns about whether the future of the ecosystem is at risk.

Brexit is still happening. With the contentious US presidential election having just been settled and the coronavirus pandemic still raging, the UK’s exodus from the EU has been slightly pushed to the background. However, the divorce will happen, deal or no deal, on December 31. For FinTech and RegTech companies, the divorce could yield new obstacles to overcome.

“Brexit could potentially create significant problems for RegTechs and FinTechs based in the UK which have a large European client base as there will be obstacles and new parameters for them in terms of selling products and services cross border within the EU,” says Remonda Kirketerp-Moller, founder and CEO of Muinmos, the RegTech company. “If the UK leaves the EU without a deal, differing EU member states will have differing requirements when dealing with the UK and this will make matters particularly complicated.”

Historically, the UK has been home to one of the most buzzing FinTech ecosystems in the world. And it’s hardly surprising that the nation is home to leading innovative companies like Checkout.com, Revolut, Monzo, Starling Bank, Onfido, Kilter, iwoca, Behavox and many more.

“The fourth industrial revolution has been driven by tech entrepreneurs,” says John Lee, president of CSS, the RegTech company that acquired AMFINE in September. “London, alongside New York, Silicon Valley and Singapore, remains one of the world’s foremost entrepreneurial locations.”

There are several key reasons for this. Firstly, London has long been one of the most vibrant financial hubs across the globe, which paved the way for innovative digital solutions. Secondly, the government and its regulators have actively nurtured the growth of the sector through regulations, support structures and regulatory sandboxes. Additionally, the UK is home to an ecosystem of investors, accelerators and incubators all eager to support startups.

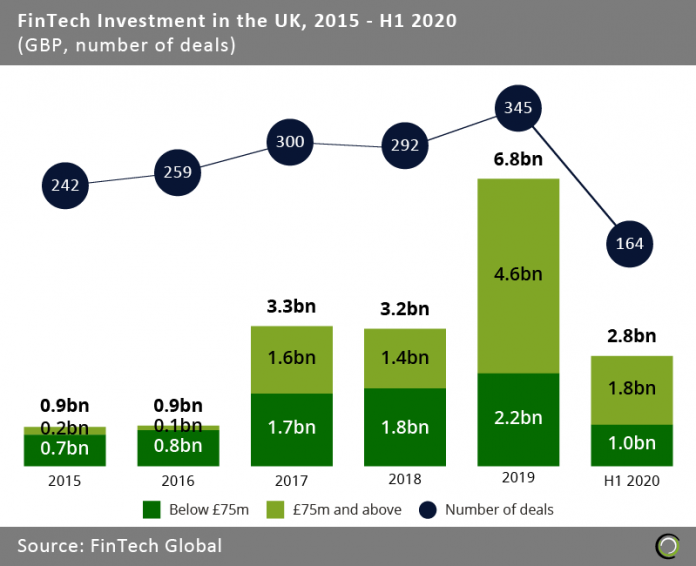

So it is easy to see why investment into the FinTech UK scene has skyrocketed in recent years. Back in 2015, only $900m were invested into the nation’s sector. Fast forward to 2019 and that figure had jumped to $6.8bn, representing a compound annual growth rate of 64.6% in those five years.

However, investors are famously weary of uncertainty. With a Brexit deal still to be finalised and the coronavirus continuing to wreak havoc on the economy, it would be expected that investment into this space would drop.

However, investors are famously weary of uncertainty. With a Brexit deal still to be finalised and the coronavirus continuing to wreak havoc on the economy, it would be expected that investment into this space would drop.

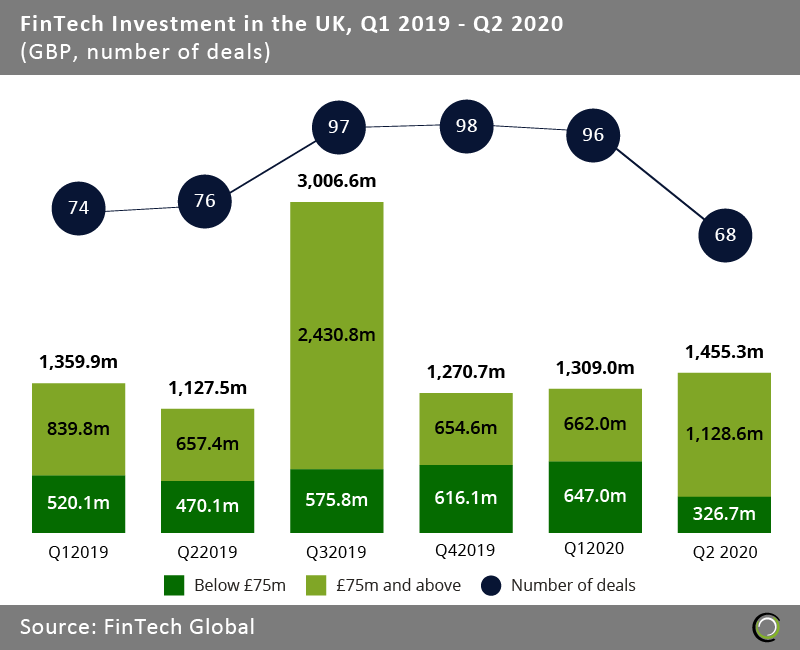

Although, an argument can be made that things are not so bleak. While cash injections into the industry have dropped since the record $3bn third quarter in 2019, investment levels in the UK have mostly stayed on the same level as the ones enjoyed during most quarters.

“For firms with a business model that has a path to revenue and profitability, there will still be plenty of equity funding available,” says Nikolai Hack, head of strategy and partnerships at WealthTech company Nucoro. “As high yielding assets are harder and harder to find, there might be even more capital available than before.”

Similarly, Kirketerp-Moller is still seeing a lot of opportunity in the RegTech sector, partly thanks to the pandemic. “The increase in homeworking due to Covid-19 restrictions has made two of the biggest challenges faced by the compliance function in financial institutions even more apparent, namely, keeping up with regulatory change and cybersecurity,” she explains.

“It is vital that financial institutions address these two areas in order to operate effectively and mitigate the risk of significant fines for regulatory or data breaches. Despite the economic impact caused by Covid-19 and potentially by Brexit, RegTechs which address either of these two areas will continue to thrive and attract significant investment opportunities.”

Hack shares a similar optimistic sentiment. “Brexit means more regulatory divergence across Europe,” he says. “For pan-European and global firms this will mean more work on the compliance front. In turn this creates more work and problems for RegTech to help solve [which means] this is bullish for RegTech on the European and global level.”

That being said, he notes that there is a risk that RegTech firms only operating inside of the UK could face one challenge: less regulations. “[The] FCA has always been on the more free reigning side of things compared to its European counterparts,” Hack explains. “Hence, for firms inside the UK and only focussed on that market, less regulatory workload could mean a reduction in the demand for RegTech services. However, the demand and need for straight through processing and end to end automation does not go away. In sum: still bullish for RegTech as a whole.”

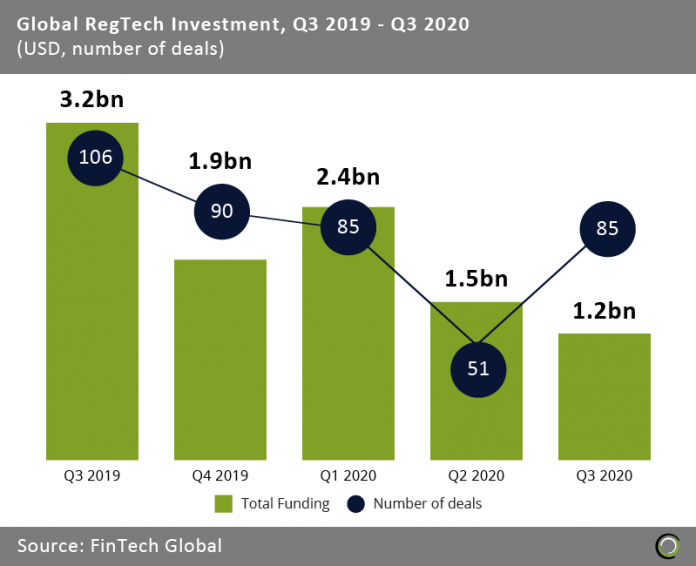

Nevertheless, there are wrinkles to this bullishness as the nation’s RegTech and FinTech firms are far from out of the woods yet. When looking at the global RegTech industry, there has been a notable drop in investment since the pandemic broke out. Only $1.2bn was injected into the industry between July and September this year, marking a five-quarter low, according to FinTech Global’s research. Slightly similar trends could be noticed in the InsurTech and the WealthTech space, although both those sectors recovered ever so slightly in the third quarter.

“The combination of Covid-19 and the uncertainty of Brexit are certainly making investors pause and re-evaluate – I think decisions from investors on FinTechs are slowing down, probably until at least early 2021,” says Kirketerp-Moller.

“The combination of Covid-19 and the uncertainty of Brexit are certainly making investors pause and re-evaluate – I think decisions from investors on FinTechs are slowing down, probably until at least early 2021,” says Kirketerp-Moller.

Other concerns have more to do with the coronavirus than with Brexit. “What could and will change the dynamics is a major economic downturn that really destroys a lot of real economic potential and spills into the FS sector through rising delinquencies and eroding balance sheets,” Hack says. “Prolonged lockdowns, quarantine regimes, etc will do that eventually.”

He adds that firms that over-leverage more and more to survive the health crisis could find that debt weighing them down. “Corporate debt levels are generally already very high and through more debt funding vehicles and cheap credit being accessible, smaller firms are going down that same route,” Hack argues.

“It means a step by step zombification of certain sectors of the economy, where firms are only alive as they can service existing debt with new cheap debt. That has a high risk of cross contamination of otherwise healthy firms that do business with zombified firms, that might eventually unable to service their debt. This is true for FinTech as much as it is for other sectors of the economy.”

So, what does all this mean? “I don’t believe the often talked about negative effects of a Brexit exodus of capital and talent in FS and FinTech do exist,” Hack argues. “The UK, in direct contrast to the continent, is still the more attractive place to open and run a FinTech, or [a] startup generally. London will keep its pole position as an ecosystem centre as well for the foreseeable future. The aspects of commercial culture, concentration of talent and access to capital are still far ahead of any place on the continent.”

In fact, he believes the startup in the nation may even get a boost from the UK’s divorce from the EU. “On top the changing dynamics create bigger and harder to overcome problems for incumbents than for challengers,” he says. “If anything, this should actually open up more opportunities for smaller firms that are more nimble and can navigate a new environment quicker.”

Copyright © 2020 FinTech Global