Investment into Australian FinTech skyrocketed last year, but why has it become so appealing? The country has seen a number of new FinTech startups launch over the past year, particularly challenger banks, with the likes of 86 400 and UP both launching in 2019. A slew of investment deals in 2020 shows this appetite for Australian FinTech is not stopping.

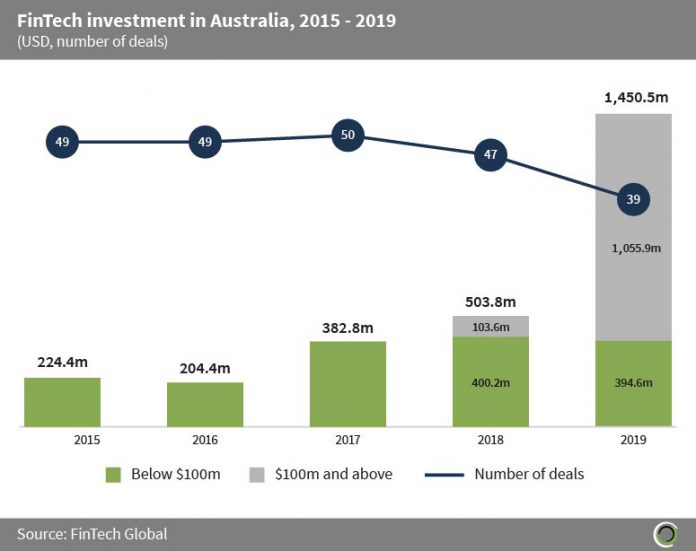

In 2019, a total of $1.4bn was invested across 39 transactions in Australia, compared to the $503m invested into the country the previous year, according to data from FinTech Global. However, despite the increase in capital, there were eight less deals completed in 2019 than in 2018. The reason capital increased so much was because more FinTechs closed deals over $100m.

The country’s FinTech sector has grown quite significantly over the past year. Back in 2015, the sector received just $224m across 49 transactions. Since then Investment has grown at a CAGR of 59.5% between 2015 and 2019. Why has the sector had such a rapid growth? It’s hard to tell what the exact cause is, but the country’s consumer data right (CDR) is definitely helping to encourage growth in the subsector.

The country’s FinTech sector has grown quite significantly over the past year. Back in 2015, the sector received just $224m across 49 transactions. Since then Investment has grown at a CAGR of 59.5% between 2015 and 2019. Why has the sector had such a rapid growth? It’s hard to tell what the exact cause is, but the country’s consumer data right (CDR) is definitely helping to encourage growth in the subsector.

CDR was announced by the Australian government in 2017 and gives consumers greater and control over their data. The regulation, like similar open banking initiatives cropping up around the world, enables customer to consent for their banking data be shared with trusted third-parties in order to access more personalised services. The goal of the regulation is to encourage competition in the market.

Fred Schebesta, CEO & co-founder of Australia-based comparison website Finder, said, “Australia’s approach to opening up data through the Consumer Data Right sets it apart from most other countries. A lot of countries are launching an open banking program to free up banking data but Australia is aiming to take that approach across more industries.” While banking data has been the first area the regulation has focused on, it will move into other industries including energy, superannuation and insurance. “Information is power and Australian consumers need tech firms to help make the most of their data,” he added.

At the start of the year, the Australian Competition & Consumer Commission (ACCC), the regulator enforcing the CDR regulation, delayed the implementation of legislation by five months. It was originally pitched for an enforcement date of February but is now being held off until 1 July 2020. With the current COVID-19 (coronavirus) pandemic and regulators taking measures to ease the shock on financial market, the date could be pushed back further. This does not mean companies are holding off on getting things ready. Earlier in the week, Regional Australia Bank became the first accredited data recipient of the CDR.

CDR is not the only initiative the Australian government has released to support the development. Late last year, it announced the Select Committee on Financial Technology and Regulatory Technology which is conducting an inquiry on how the two industries (FinTech and RegTech) have developed and what can be done to help them grow even more. A finding will be issued in October 2020.

Some of the key things it is looking into are what the sectors mean for consumers, barriers for entry, the progress of FinTech facilitation reform and the benchmarking of comparable global regimes, how RegTech is currently operating and how it can help improve compliance and cut costs. Finally, it will explore how effective current initiatives to boost the industries have been.

Schebesta said, “I’m super excited about the recommendations the Select Committee will make in their final report later this year. We have worked closely with the Committee and we know that there are a lot of key policy makers that will take these recommendations very seriously.”

There is a lot of optimism towards the CDR regulation and the opportunities it presents Australian FinTech. Schebesta said. “The Consumer Data Right is a great first step towards improving access to financial data and will encourage great innovation in financial services in Australia.”

Brian Costello vice president of data strategy and strategic solutions at data aggregator Envestnet|Yodlee said, “[It] will increase the engagement, empowerment and protection of citizens already part of the highly innovative consumer-permissioned data ecosystem.” Despite the optimism, there are still some kinks that will need to be ironed out, he said. One of the issues is that the regulation will not have an immediate impact on the market, but may be a gradual transition to new and improved services

Open banking in Australia will not have overnight results and Robert Bell, the founder of newly launched digital bank 86 400, believes that the benefits of the CDR regulation will only be felt after two years of it being implemented. Speaking to Which-50, he stated that a lot of hype is being put on the regulation, but when it is enforced only limited subsets of data will be available from four financial institutions will be available. It will take time until there is a more comprehensive dataset available, and until then, open banking will not be as impactful as it can be.

The regulation could help FinTech companies attract more customers. The country’s digital bank space has seen a lot of uptake over the past couple of years. 86 400 and Up both launched their services to the market, while DayTek Capital pitched itself for a 2021 launch. There has also been a lot of financial support going to these digital services. Last year, 86 400 secured a $100m funding round, Xinja netted AUS $2.6m in crowdfunding while Judo Bank secured $270m and then a further $350m in 2020.

One of the reasons digital banks could be seeing a rise in activity and attention may be down to the diminishing trust towards traditional financial institutions in Australia. In 2017, the Australian Royal Commission into Misconduct in the Banking, Superannuation and Financial Services Industry was launched following several claims of misconduct in the banking sector spread across the media. One accusation was the Commonwealth Bank of Australia had been accused of ignoring money laundering for drug syndicates, terrorism financing and statutory reporting. A final report was released detailing 76 recommendations to minimise risk of bad behaviours in the banking sector. With the opportunities of CDR, more people could move towards FinTech providers.

Whether or not it will help increase traffic to FinTechs, Schebesta believes there will be a spike in interest on digital services generally. He said, “I expect this new open banking world in Australia will lead to a rise in the popularity of personal finance and accounting apps. Everything will operate from your phone and innovative companies will be able to predict what consumers need, provide more automated affordability checks, and money-saving prompts. This is the one that I’m most excited about because we’re building this future right now with the Finder app, which aggregates your banking products and automates comparison.”

This does not mean the regulation is without work and more can be done. Extending the reach of the regulation to reach other industries such as insurance or retirement is a common theme. There are also other changes that could also be made to improve the legislation. “We also need to start looking at how we can include “write-access” into the Consumer Data Right legislation. The current “read-only” access gives consumers powerful insights about the way they spend money, but it’s “write-access” CDR that will give consumers the power to act on these insights quickly,” Schebesta said.

Copyright © 2020 FinTech Global