Challenger banks are on the rise around the world, but things are not always running as smoothly as they could.

Digital banking startups are challenging the incumbents around the world. While challenger banks in the UK have raised hundreds of millions of pounds over the past decade, 2019 made it clear that similar growth can be expected around the globe.

For instance, Pride Bank has been launched to cater to Brazil’s underserved LGBT population, UK challenger bank Tandem announced plans to open in Hong Kong and in the US, startups like HMBradley and Chime are going from strength to strength.

Even Australia, which has traditionally been slow to accept new banking companies, has now opened up for challenger banks to establish themselves in the sector by introducing a new type of banking licence. A slew of startups, including 86 400, Up and Judo, has jumped on the opportunity to cut out a piece in the market for themselves.

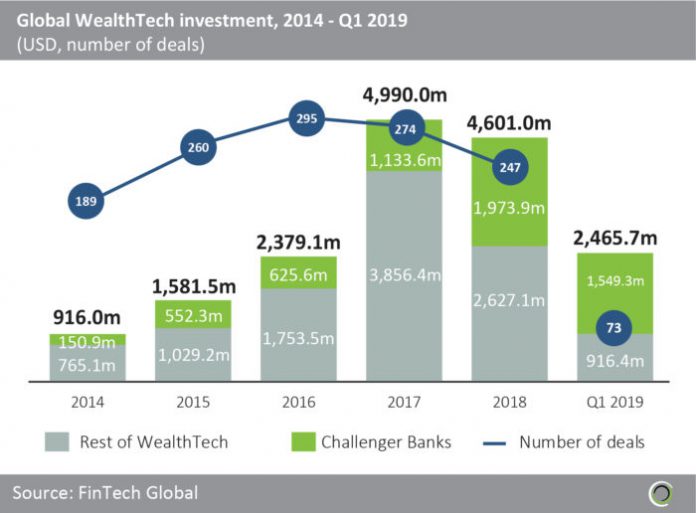

With this background, it is easy to see why the sector is estimated to be grow to be worth $301bn by 2025. This notion is backed by FinTech Global’s research which showed that the sector is annually attracting more and more investment. In 2014, $150.9m was invested into the sector. That number grew to $1.97bn in 2018.

While the sector is going from strength to strength, the last year proved that things do not always run as smoothly as the savvy entrepreneurs behind the enterprises hope.

Here’s seven examples of when things did not go as planned.

Regulators criticised N26

2019 was the year when German challenger bank N26 officially announced it was launching in the US. However, it was also the year the German banking regulator BaFin published a laundry list of shortcomings the FinTech scaleup was urged to amend to prevent money laundering and terrorism financing.

The list included calls to remove backlogs in IT monitoring, establish process descriptions and workflows in writing and to reidentify a specified number of existing customers. The challenger bank was also criticised for clients under distress struggling to reach customer services.

In March, Der Spiegel had reported that several customers had been locked out of their accounts after falling victim to phishing attacks, Yahoo Finance reported.

N26 responded that it had already amended some of the issues and was working on the rest.

Revolut customers left unable to use the unicorn’s services

By most accounts, UK challenger bank Revolut had a great year. From seeing its user numbers boom in Romania and going live in Singapore to rolling out a direct debit service in the UK and announcing it would add 3,500 new employees to its global workforce as it planned an international expansion, 2019 had no shortage of achievements accomplished by Revolut.

But everything did not run 100% according to plan. FinTech Global revealed in October that Revolut customers were facing some issues logging in to the digital bank’s platform.

When FinTech Global reached out to Revolut, the challenger bank stated, “We are currently experiencing a technical issue that is preventing some customers from logging into the app. Card payments and ATM withdrawals are working as normal, and our engineers are currently working on restoring access as soon as possible. We’re really sorry for the inconvenience caused to our customers, and we are keeping them updated every step of the way.”

Revolut’s spokesperson did not answer any questions about what the outage was due to or if it believed it was part of a hack.

The challenger bank is hardly alone in having faced digital service outages. In November, TSB Bank stated some of the transactions into customers’ accounts had been delayed. During Black Friday, NatWest and Royal Bank of Scotland (RBS) crashed, preventing customers to make the most of the shopping holiday deals.

Future failures from financial services firms to provide those sort of digital services could face big penalties as British lawmakers are seemingly gearing up to amend the Senior Managers and Certification Regime to make financial services organizations take responsibility for any digital service outage.

Monzo closed its premium offering just months after unveiling it

In April 2019, Monzo unveiled its premium membership. For just £6 per month, customers would be able to access a slew of benefits, get different coloured cards and the chance to buy add-ons like travel insurance and fee-free foreign ATM withdrawal.

Then Monzo suddenly scrapped the service in September, admitting that “things just haven’t gone the way they should with Monzo Plus so far this year.” Monzo did hint that a new version might be in the making as the engineers were “going back to basics and starting from the beginning.”

The cancellation of the premium accounts raised concerns from investors who were yet to see a return on their investment from the scaleup, which was still to make a profit.

Competitors Revolut and Curve had both been able to launch successful subscription services.

Still, Monzo was still hailed as one of the most recommended brands in the UK in November, according to a list complied by MoneySavingsExpert.com.

That time Chime went down

Millions of Chime’s customers were unable to access their money for over 24 hours when the US digital bank’s services went down in October.

Soon, Chime’s social media channels were filled with complaints from people unable to pay bills, buy groceries or run simple errands.

It even got the point where some speculated something more nefarious than a simple technical glitch was behind the outage. Some bluntly stated that they thought Chime had suffered a hack attack and accused the bank of now trying to cover it up.

Chime denied it had been breached and maintained that all data was still safe.

“We can assure you all account information remains secure,” Chime’s Twitter account replied to one of these allegations. “No personal information or transaction information has been affected during this outage. We have identified the issue and are working to resolve it ASAP.”

This setback did not hold Chime back from announcing the closure of a $500m Series E round at the end of 2019, potentially pushing its valuation to $5.8bn, tripling its $1.5bn valuation from earlier in the year.

Metro Bank horrible year

2019 was not Metro Bank’s year. Founder Vernon Hill’s startup made a lot of headlines when it became the first high street bank to launch in the UK in over 150 years in 2010. Understandably, expectations were high. For the first eight years it seemed as if Metro Bank would live up to them. In March 2018, it was trading at a record high of £40.18 per share. But things would turn sour fast in 2019.

Metro Bank’s bad year began in January when it revealed a £900m accounting error concerning the riskiness of a string of property loans. The news shocked the investors and sent the scaleup’s into freefall. In the beginning of February, Metro Bank shares were traded at £12.

But that was not the last setback. In May, Metro Bank faced social media rumours about customers’ money not being safe at the bank, which led to many people rushing to the bank to empty their accounts and safety deposit boxes.

Metro Bank failed to drum up interest for a bond sale in the beginning of September, again causing shares to drop to £1.56 per share.

Things looked up slightly at the end of the month when Metro Bank succeeded in raising £350m in a second bond sale.

Following this smattering of negative headlines, Hill announced he would leave the company by the end of 2019, despite having previously stated that the would “probably die” rather than exiting the business.

Still, 2019 was not all bad news for Metro Bank. It ended the year in with a £15m deal that saw James Gilinski Bacal, a Colombian investor, buy a 4.3% stake in the business.

In December, the company announced that it would launch a cash delivery service named MCash.

Concerns rose that Starling Bank would be unable to live up to SME funding promise

Anne Boden’s challenger bank had a ton of achievements in 2019. Starling Bank ended the year with over one million users on its platform, closed a £30m funding round at the end of October on the back of the £75m round raised in February and aimed to break even at the end of 2019.

However, the company faced criticism in early December when it was revealed it seemed unlikely to live up to its promise of investing £913m to SMEs by 2023.

The money was pledged as part of an investment from the Royal Bank of Scotland. Starling Bank had only injected £782,000 to small businesses since receiving the money in February, representing 1% of the money promised.

People were understandably concerned that Starling Bank would be unable to live up to its promise.

Starling Bank responded to these worries by saying that this was “only the beginning” of the company’s four-year commitment.

Monzo customers left unable to access their money

In July, Monzo had some issues with its services. More specifically, users were unable to access their accounts. Others, who could log in were shocked to see incomplete and outdated information on their accounts.

Once made aware of the issue, Monzo spent the next couple of hours trying to get things back on track.

On Tuesday July 30, the bank stated, “Due to an incident yesterday afternoon, we’re working hard to answer a number of urgent queries. In the meantime it might take us a little while to get back to you.”

Copyright © 2020 FinTech Global